Glenn Beamer

A retrospective analysis of the employee purchase of the Weirton Steelworkers by 11,000 union workers brings into relief the critical role collective bargaining agreements had in motivating the original parent corporation, National Steel, to seek an alternative to closing the plant and subsequently to enabling employees to balance their desires for secure incomes and pensions with the company’s financial obligations. There are three critical lessons from Weirton’s experience. First, labor progressives created a political context that enabled the union leadership to leverage concessions from National Steel. Second, democratic practices instituted by the employee stock ownership plan (ESOP) and the Independent Steelworkers Union’s collective bargaining agreements enabled worker-owners to secure incomes and pensions. Third, collective action and collective interests created and sustained majority support for the ESOP. Had employees acted

individually it is unlikely they would have sustained employment and pensions for twenty years.

Two decades have passed since the 11,000-member Independent Steelworkers Union created the largest employee-owned company in the United States by collectively purchasing the Weirton Steel works from the National Steel Corporation. When the workers purchased the plant in 1983, the United States steel industry was in the midst of a three-decade-long collapse in which over two-thirds of its one-half million manufacturing jobs would disappear. In the two years prior to the Weirton purchase, steel producers had closed scores of plants in Pennsylvania, New York, and Ohio.(1) At the time of the employee purchase Weirton’s collective decision was exceptional because it was one massive integrated steelworks that was not closing, yet the workers’ purchase of Weirton Steel has significance beyond the media attention it attracted 23 years ago.2 Weirton workers’ experience reflects labor’s potential as a political and economic institution to secure its rank-and-file members’ jobs and pensions. A retrospective analysis reveals the substantial economic security the employee purchase provided and continues to provide as its legacy. Only by acting collectively were workers able to collectively and democratically balance their company’s needs for lower costs with their collective goal of securing pensions.

In the aftermath of the employee purchase critics from both the left and right criticized Weirton’s union, its management, and its workers. Scholars on the left focused on the constrained levels of democratic capitalism in which employees found their managerial prerogatives limited.3 From the right, critics charged that Weirton Steel’s owner-workers overindulged themselves with favorable profit-sharing, an over-emphasis on job preservation, and insufficient efforts to raise capital.4 Both perspectives misperceive the steelworkers’ goals that were paramount during the

employee ownership campaign. The appropriate basis by which to evaluate Weirton’s experience is neither a standard of workplace democracy nor a standard of economic efficiency. We should evaluate Weirton’s experience based upon the shared goals that prevailed among workers during the employee stock ownership plan (ESOP) campaign, sustaining jobs and securing pensions, and we can evaluate Weirton’s experience relative to other United States steelworkers whose companies were sold to new owners during the 1980s and 1990s.

Archived records and interviews with involved individuals reflect that the paramount concerns shared by a substantial majority of workers were the related dimensions of sustaining jobs and securing defined benefit pensions.5 The collective bargaining agreements between the Independent Steelworkers Union and National Steel provided labor with economic power with which to negotiate price concessions and pension and benefit protections for workers and with political cohesion with which to create majority support for the employee purchase.6

Weirton’s experience provides three lessons about the role of collective action in creating economic security. First, labor progressives created sufficient political pressure that the local union leadership negotiated improved pension protections for its workers. Second, democratic practices relating to employee ownership and collective bargaining enabled workers to secure their incomes and pensions.7 Although Weirton Steel did not become the arena of workplace democracy that some envisioned, workers made critical decisions about their company’s practices

democratically and retained sufficient control for sufficient time to secure their pensions. Third, Weirton steelworkers succeeded in sustaining jobs and income security because they acted collectively and retained their collective interests in the company’s fortunes. Had their shared commitments been diluted workers might have not have balanced their individual, sometimes competing, interests, with the company’s financial needs for two decades. These lessons are particularly relevant for communities responding to deindustrialization and globalization.8

This paper proceeds in three sections. The first section presents a brief history of the Weirton Steel works and the Independent Steelworkers Union. In the second section, I trace critical collective decisions that workers voted upon as both union members and company owners. These votes enacted policies that sustained jobs, protected and funded the defined benefit pension plan, and attracted capital investments that modernized the steel mill. The third section analyzes the returns workers received in exchange for their wage and benefit concessions that financed

their plant purchase. This analysis demonstrates that Weirton workers collective actions resulted in substantial income gains for themselves and their community.

Weirton’s experience reflects the interaction of public and private policies.9 The United States Employee Retirement Income Security Act (ERISA) of 1974 provided the public regulatory framework that obligated National Steel and the Weirton ESOP to honor their pension commitments to Weirton steelworkers. Like the industrywide Experimental Negotiating Agreement, which covered steelworkers at the ten largest United States steelmakers, the National Steel—Independent Steelworkers Union (ISU) contract instituted the Rule of 70/80.10 The Rule of 70/80 provided

pensions for employees over age 55 whose combined age and years of service equaled 70 or greater. Employees younger than age 55 were eligible to receive pensions if their combined age and years of service totaled 80 or more. Employees forced to retire because of plant or department closures became eligible for ‘Shutdown’ pay equal to US$400 per month until they reached age 62. Shutdown pay supplemented pension payments and substituted for federal social security benefits which retirees could receive once they became 62 years old. The Rule of 70/80 was the most common of several ‘Magic Number pensions,’ which were collective bargaining provisions that provided economic security for hundreds of thousands of steelworkers who had gone

into the mills in their late teens and early twenties. Magic Number pensions provided substantial economic security when plant closures began in the mid-1970s and as layoffs and shutdowns continued through the 1980s. From the company managers’ perspective, Magic Number pensions created tensions among shedding employment, reducing labor costs, and retaining productive capacity.11

Steelworkers’ pensions connected younger and older workers and gave them common cause to balance their goals and the company’s financial obligations. Pensions embedded economic power in the union and reconfigured the decision-making calculus of plant managers.12

The Weirton ESOP, 1982–84

Since the 1950s Weirton Steelworkers had collectively bargained through their locally based Independent Steelworkers Union (ISU).13 Unlike their counterparts at other US steel producers, Weirton’s steelworkers were not represented by the UnitedSteel workers of America (USWA). In 1950 the National Labor Relations Board cited National Steel’s management for contempt because of its union interference. By this time USWA had organized most of the steel plants in the United States and there had Labor History 279 been nationwide strikes in 1946 and 1950. During these strikes Weirton’s workers continued making steel and National Steel paid premium wages to keep labor peace. In the aftermath of the NLRB ruling, Weirton workers organized their stand-alone Independent Steelworkers Union as their collective bargaining agent. Despite another decade of efforts, the USWA never obtained the necessary 3,000 or more Weirton

steelworkers’ signatures that it needed in order to contest the ISU’s institutional role in the community.14

Because they had not joined the United Steelworkers of America, National Steel paid wage premiums to Weirton workers through the 1970s. Weirton’s steelworkers had worked through five nationwide steel strikes during the 1940s and 1950s, and both workers and the company profited by producing and selling steel when other companies ceased production. However, this arrangement became less advantageous during the 1970s when the USWA and the ten largest US steel producers agreed to a no-strike clause in the collective bargaining agreements. Without strike-induced sales and profits from Weirton, the wage premium that had discouraged Weirton’s workers from joining the USWA became an unneeded expense.

In 1908 Ernest Weir moved his newly formed steel company to the hamlet of Holiday’s Cove, West Virginia and founded the town of Weirton and the Weirton Steel Company. The municipal government and steel company often operated jointly with company managers paternalistically providing for the community’s needs and the city and county governments catering to the company.

In 1929 Weir merged his Weirton Steel Company with Great Lakes Steel, which was located in Michigan, and an amalgam of smaller steel processors to form the National Steel Corporation. Weirton Steel operated as a distinct division of the larger corporation. By the time of the employee purchase in the early 1980s 8,000 active and 3,000 laid-off laborers remained in the larger community, which included Brooke and Hancock Counties in West Virginia, and Jefferson County in Ohio.15

Because of its wage premium, new competitors, and market contractions the Weirton plant became the least profitable and most vulnerable of National Steel’s major facilities. In 1982 National Steel announced it would close the 11,000- employee Weirton Steel works unless local managers and laborers agreed to buy the mill.16 At the time of this announcement, steel companies had laid off nearly 115,000 hourly workers, and industry leaders such as US Steel and Bethlehem Steel were permanently closing plants that had employed scores of thousands of workers.17 In a community with approximately 125,000 citizens Weirton Steel provided as many as 13,000 jobs as late as 1974. Its central place in the community made the ESOP campaign a focal point of community politics for more than two years.18

By early March, National Steel began negotiating with the Independent Steelworkers’ Union, which represented over 8,000 hourly wage employees.19 Among its motivations for proposing the employee purchase was the liability that the Rule of 70/80 would have triggered if large portions of the plant closed. By January 1984 the ISU and National Steel successfully negotiated a sale in which the employees purchased the mill via an employee stock ownership plan.

The Rule of 70/80 and shutdown benefits created a fixed cost of closing plants and furloughing employees. For a 50-year-old mill worker with 30 years of service the nominal cost of a shutdown pension supplement was approximately US$57,000. The added years of pension payments and insurance benefits created a liability of US$100,000–250,000 per employee (figures are in 1983 dollars).20 Potential liabilities triggered by the Rule of 70/80 amounted to nearly US$30 billion among the ten largest US steel companies. These potential liabilities discouraged steel firms from

closing mills, and mills with more workers were better insulated against shutdowns.21 At Weirton, National Steel faced US$300 million in pension and severance liabilities, assuming it could retain 1,500 senior workers.

Because of the Rule of 70/80 and other legacy provisions, National Steel faced shutdown charges as high as US$770 million to close its Weirton works, an amount that would have placed the corporation in bankruptcy.22 If workers rejected the ESOP, National Steel planned to ‘harvest’ the Weirton works and keep approximately 1,500 of the 8,000 workers. This alternative would have minimized shutdown costs. By retaining its finishing mills National Steel could shift senior employees into the remaining jobs and lower shutdown liabilities by approximately US$75–100 million.

The 1,500 remaining workers would have had at least 28 years’ seniority and approximately 95 percent of them were eligible for Rule of 70/80 pensions and shutdown pay.23 Had the workers done nothing and National Steel entered bankruptcy, workers and retirees would have lost life and health insurance benefits. The vast majority of active and all laid-off workers would have received reduced pensions after age 65. By purchasing the plant, workers sustained their pensions and became eligible to collect them as early as age 45.

Weirton’s Independent Steelworkers Union and Weirton Steel division managers formed a Joint Study Committee to recommend options regarding the employee purchase.24 The committee explored three options to purchase the mill: (1) issuing stock that employees would buy outright, (2) using vested pension benefits as collateral and issuing bonds, (3) and using compensation reductions to build equity in a new company.25 The third option became the only viable option after Joint Study Committee members assessed the two former options as too risky.26 The ISU’s

proposed ESOP shifted risk away from workers and onto National Steel. Weirton’s workers pledged future earnings and not their current pension fund and did not risk losing pensions vested under service to National Steel.

In contrast to Weirton’s ESOP, 500 members of the United Steelworkers of America terminated their pension plan when they created the South Bend Lathe ESOP in 1975. The former parent corporation, Amsted Industries, presented employees with a take-it-or-leave-it proposal to adopt an ESOP or face a plant closure. These workers effectively capped their pension benefits as if their plant had closed. In 1983, union workers at Rath Packing Company voted to terminate their pensions and then ceded ownership control of their company.27 By both terminating

their pension plan and ceding ownership, the Rath workers lost their financial leverage, plant ownership, and collective goal to secure pensions.28 These workers’ experiences contributed to skepticism among many Weirtonians about ESOPs, and the ISU leadership and the Joint Study Committee responded to these workers’ experiences as they developed their political and policy strategies.

Progressive laborers and community labor activists became the primary organized opponents of the ESOP. Many older workers were deeply skeptical about the ESOP and perceived their interests were better served by remaining with National Steel’s ownership of the mill.29 Younger workers and more militant area labor leaders formed the Rank and File Committee (RFC) and argued that there were several alternatives to employee ownership. A 12-year veteran of the mill, Tony Gilliam, became the leader of the Rank and File Committee along with a second Weirton

steelworker, Steve Bauman, who was laid off from the mill. A labor activist from nearby Youngstown, Ohio, Staughton Lynd, served as legal counsel for the RFC and a Yale business school graduate student provided financial consulting.30 In previous plant-closing fights Lynd had sued companies to enjoin them from closing steel mills. Other members of the RFC had been active in community groups promoting antipoverty and social justice.31

The RFC’s alternatives included suing National Steel to continue operating the plant or seizing control of the plant under the local governments’ rights of eminent domain.32 These progressive politics became the dominant threat to an eventual collective community decision to purchase the steel works.33 Despite Lynd’s skill at organizing and advancing litigation that challenged various dimensions of the ESOP campaign and the ISU’s democratic practices, many Weirtonians recalled being skeptical of the RFC because Lynd was from outside the community and because his efforts in Youngstown had not forestalled mill closures in that community. The Rank and File Committee voiced concerns with several areas of the ESOP

negotiations and established a ten-point platform.34 The Rank and File Committee advocated increased worker participation including a union-wide vote on the final ESOP plan that enfranchised laid-off laborers.35 The committee highlighted pension issues twice on its agenda. It promoted an ESOP with a pension plan and insisted that National Steel honor its prior pension commitments.36

A Joint Study Committee report indicated that to remain viable the employee-owned Weirton Steel would have to reduce compensation costs. The report recommended workers accept a 32 percent compensation reduction.37 The wage concessions were to create sufficient revenue such that the Weirton ESOP could repay loans for the plant’s physical assets, establish a new pension plan, and create a pool of funds for capital projects. Many workers were shocked at the size of the reductions and opposition to the ESOP gained strength for a time.38

In response to growing ESOP opposition the Joint Study Committee responded both substantively and strategically. Substantively, ISU President Walter Bish convinced National Steel’s managers to retain responsibility for health and life insurance premiums for workers who had already retired from the Weirton division. National Steel’s managers had argued that these costs were to be paid from the plant’s ongoing operations and as such should be transferred along with the plant’s physical assets. Bish and the Joint Study Committee effectively argued that National Steel had obligated itself to these responsibilities in prior collective bargaining agreements. Because other steel companies were involved in litigation about retirees’ health and

life insurance, neither side knew whether US federal courts would eventually hold steel companies responsible for these obligations.39 Regardless of National Steel managers’ expectations, the Joint Study Committee succeeded in convincing National Steel to accept continued responsibility for retirees’ benefits. This concession lowered workers’ five-year financial commitment from approximately US$320 million to a far more palatable US$193 million, or about 20 percent of their wages and benefits.40 According to three former union stewards and a former

communications manager, the concession was important politically because Bish and the Joint Study Committee could credibly claim that they had decreased concessions and effectively represented workers.

Strategically, the Joint Study Committee relented on its position that only active employees could vote on the ESOP proposal and collective bargaining changes. This change brought younger workers into the political dynamic in greater numbers. In turn pro-ESOP labor leaders began to focus on long-term income security to offset the Rank and File Committee’s statements that jobs could be retained without concessions.41

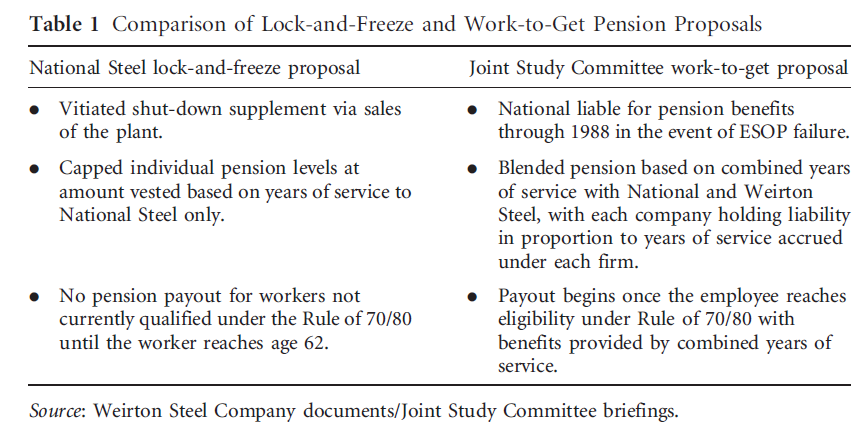

The principal new focus of the ESOP campaign became worker pensions. ISU President Walter Bish and the Joint Study Committee leveraged National Steel’s management from its ‘lock-and-freeze’ pension proposal to the ‘work-to-get’ proposal. Under lock-and-freeze National Steel’s pension liability would have been bounded at its obligations on the date of transfer. Middle-aged employees who had not yet qualified for Rule of 70/80 pensions and shutdown benefits would have become ineligible for pensions until age 62, when they would receive more modest

pensions.

Under the work-to-get proposal National Steel and Weirton Steel shared pension liabilities for employees in proportion to the employee’s service to each company. A 50-year-old employee with 20 years of service to National Steel and 10 years service to Weirton Steel would qualify for a Rule of 70/80 pension. National Steel was to be liable for two-thirds of the pension payments and Weirton Steel was to be liable for one-third. If an employee had 12 years of service with National Steel and 18 years of service with Weirton Steel, National Steel would pay 40 percent of the employee’s pension and Weirton Steel would fund 60 percent. Table 1 compares the lockand- freeze and work-to-get pension proposals.

Had National Steel succeeded with its lock-and-freeze position, it would have eliminated a sizable portion of its legacy costs. As former National Steel workers reached retirement age they would have received severely reduced retirement benefits. For example a 48-year-old employee with 30 years of service would have been one year away from qualifying for a full pension, but would have to wait until age 62 to receive a more modest pension. Under the work-to-get plan such an employee would have become eligible for full retirement after one additional year of

service to the new Weirton Steel. The work-to-get proposal sustained the Magic Number component of the steelworkers’ existing collective bargaining agreements and triggered higher pension benefits at earlier ages.42

When asked about the ESOP’s uneven political support Bish replied that the pensions became the central issue around which support and opposition crystallized. In discussing the importance of pension arrangements to the ESOP, Bish recalled,

As far as the pensions were concerned . . . that was the number one priority—that we protect them . . . the pensions were kept intact and any time we had (as service) with National Steel when the deal went through; that would count toward our pensions with the new Weirton Steel. That put a lot of people’s minds to rest.43

As a political response to the Rank and File Committee, the work-to-get proposal bonded older and younger workers and created a shared economic interest. For older workers even a few years of operation by an employee-owned Weirton Steel would enable them to qualify for Rule of 70/80 pensions. For younger workers the ESOP became the most credible means to retain and build upon the service benefits they had accrued with National Steel. A 1983 survey of Weirton’s workers estimated that 92 percent of 3,000 laid-off workers favored the ESOP.44 By enfranchising these workers for the ESOP vote, Bish and the ISU stewards tapped into a huge trove of pro-ESOP votes.

Because National Steel restricted its negotiations to the Joint Study Committee and never recognized or negotiated with the Rank and File Committee, Tony Gilliam and Staughton Lynd were unable to reassure workers that any of their proposals could be institutionalized. Nevertheless, the Rank and File Committee credibly threatened to derail the ESOP via litigation in federal courts. Several former steelworkers and community members, who both supported and opposed the Rank and File Committee, recalled that its activities and earnestness provided Bish and more

moderate labor leaders with leverage with which to negotiate a favorable sale agreement with National Steel.45

The work-to-get provisions substantially increased workers’ pension values by advancing eligibility for pension benefits and by blending service accrual from National Steel and the Weirton ESOP.46 Workers became particularly committed to retaining their service because of the ‘triggers’ that caused pension values to jump substantially when the Magic Number combinations of service and age equaled or exceeded 70 and 80.

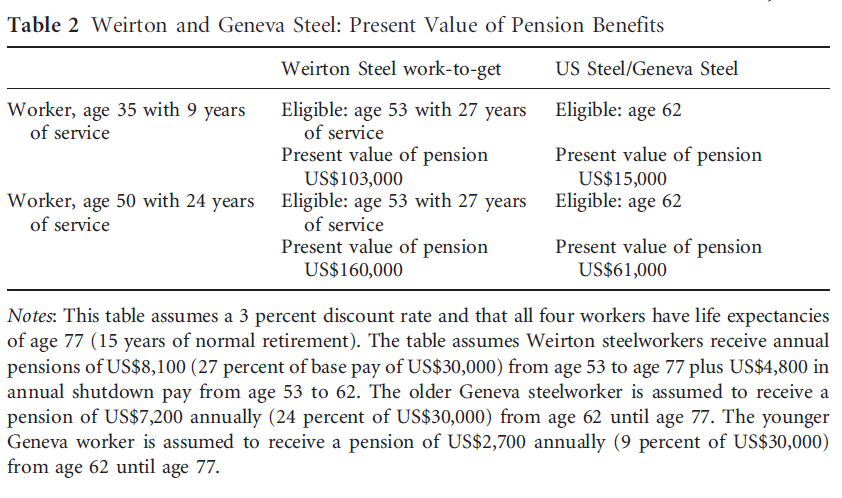

We can better estimate the extent of Weirton’s community benefits by comparing Weirton’s ESOP with Geneva Steel, a steel mill in Provo, Utah that United States Steel sold to private investors in 1987. In this latter plant sale labor gained no ownership and United States Steel froze pension benefits on the date of transfer. The new owners, Basic Manufacturing Technologies, switched from a defined benefit plan insured by ERISA to a defined contribution plan for which workers had no insurance.47 By estimating the present value of pension benefits for the two communities we can compare the relative economic value to workers. Table 2 illustrates the relative positions of Weirton and Geneva steelworkers. In addition to the relatively superior pension values, Weirton workers’ wage concessions of approximately US$5 per hour compared favorably with Geneva workers agreement to concede US$7 per hour in wages and benefits.

By adopting the work-to-get plan the ESOP significantly lowered the age at which laborers could claim their pensions, which in turn increased pension values. By instituting a lock-and-freeze pension upon its sale of the Geneva Steel Works in Provo, Utah, US Steel limited its legacy costs and deferred those costs for employees who had not qualified for pensions under the Rule of 70/80.48 Depending upon a worker’s age, the US Steel plan provided one-sixth to one-half of the present value of the Weirton Steel work-to-get plan.49 Whereas a 35-year-old worker in Geneva would have to wait 27 years to collect about US$175 per month, a Weirton employee covered by the work-to-get provision would become eligible for a Rule of 70/80

pension at age 50 and would receive approximately US$1,150 monthly.50

To attract younger workers’ support the Joint Study Committee designed the ESOP to preserve recall rights for laid-off workers. The employee-owned Weirton Steel extended recall rights beyond the 24 months provided for by its collective bargaining agreements. When the company did not restart some departments that had been idled during the 1982 recession, recall extensions enabled laid-off employees to return to the mills as positions became available. Walter Bish recalled,

When we went through the ESOP in 82 and 83, with 3000 on lay-off, I really had one goal and that was to give every active employee at Weirton and everyone on lay-off the chance to come back and work for Weirton and qualify for a pension . . . And we made that goal in ’97. 51

The final ESOP agreement included a failsafe provision. This provision stipulated that if the ESOP Weirton Steel failed financially prior to 1989 pension liability would revert to National Steel. This five-year failsafe provision ensured that National Steel could not lay claim to the ESOP Weirton pension fund in the event the new Weirton Steel entered bankruptcy.52 Because workers at other companies had been forced to sue former employers for pensions that had been transferred among corporate entities and their subsidiaries, many Weirton steelworkers remained concerned that National Steel was engineering the ESOP only to avoid Rule of 70/80 obligations. The five-year fail-safe provision obviated any intentions National Steel may have had to reacquire the Weirton ESOP’s assets, force their liquidation, or absolve itself of its pension responsibilities.53 This provision helped generate support among middle-aged workers who were close to qualifying for Rule of 70/80 pensions and may have been willing to gamble that staying with National Steel while it harvested the mill would permit them to qualify for their pensions. The fail-safe provision obviated middle-aged workers’ reasons for gambling with such a strategy.

In comparison with Weirton’s steelworkers, union workers at other threatened steel mills in the United States conceded greater wages, lost jobs, and recouped less economically. At the Geneva plant in Utah, USWA members agreed to wage cuts of US$7 per hour, lowering compensation from US$25 to US$18 per hour in 1987. Geneva workers agreed to a lock-and-freeze pension plan that terminated their defined benefit plan under US Steel and introduced a defined contribution plan under the new owners, Basic Manufacturing Technologies.54 Prior to the plant sale

the USWA had proposed an employee buyout that US Steel’s managers declined to negotiate. Because the Geneva plant represented only 2,000 of US Steel’s then 40,000 unionized workers Geneva workers had far less economic leverage than steelworkers in Weirton. 55 The Weirton division of National Steel accounted for nearly half of that corporation’s unionized workforce, and US Steel could better absorb shutdown charges than National Steel.

In Johnstown, Pennsylvania, workers agreed to a 50 percent reduction in wages, from US$24 to US$12 per hour, as a condition for regaining jobs at the former Bethlehem Steel mills.56 In return for US$33 million in state and local government assistance, new investors promised to restore 800–1,000 of the 1,800 jobs that were lost when the mills closed in 1992. The new managers recalled only 400 workers, and all these workers lost their jobs in 2000 after the successor company, Bar Technologies, merged with another steel company.57 Like Weirton’s workers, Johnstown steelworkers had been granted an equity stake in Bar Technologies, but they only owned 25 percent of the stock and had no means by which to avert the company merger that presaged the end of their jobs. By minimizing economic concessions, fusing workers’ interests via the work-to-get and five-year failsafe provisions, and extending voting and recall rights for laid-off workers, the ISU leadership created substantial support for the Weirton ESOP. In September 1983, ISU members approved the ESOP in a series of votes.58 The first vote of 6,136 to 872 approved the new concessionary contract between the ISU and the newly independent Weirton Steel. The second vote, 5,942 to 1,036, amended the hourly workers’ existing contract with National Steel to stipulate that the transfer was not a shutdown and would not trigger extraordinary benefits. The final vote of 6,203 to 744 approved the establishment of the ESOP.59 Pro-ESOP labor leaders succeeded in focusing Weirton on jobs and pension security. This focus remained for the next two decades during which thousands of workers secured federally insured defined benefit pensions.

The Weirton Steel Experience, 1984–2003

Following the votes that created the ESOP, the new company formed a board of directors that included Walter Bish, the ISU’s counsel David Robertson, and Irving Bluestone. Bluestone was a pro-labor university professor and had been active in the United Autoworkers. The company’s management appointed three directors and the ESOP’s creditor banks were allotted six seats on the board. Although stock would be allocated on a one worker one share basis, the company’s directors were likely to give priority to satisfying its loan obligations.60 Beyond the newly constituted board of directors, the company’s management changed little following the employee’s acquisition.

For twenty years Weirton workers balanced competing demands to recoup concessions from the 1983 collective bargaining agreement, sustain employment and pensions, and generate sufficient capital to modernize their plant and remain economically competitive. In order to advance all three goals the worker-owners traded ownership and control of the company for jobs and retirement benefits. In a sequence of votes Weirton’s workers articulated their calculated willingness to cede ownership in the company in exchange for wage and retirement improvements. For those who fault Weirton for a lack of workplace democracy these votes were too few and far between.61 For Weirton’s capitalists’ critics the substance of the votes— wage and pension increases and limits on diluting worker-ownership—demonstrated workers’ unwillingness to concede sufficient economic resources.62 From workers’ perspectives the votes secured government-insured pensions while preserving their control of a struggling company in an increasingly competitive industry.

There were six democratic decisions that enabled the employee-owned Weirton Steel to provide secure pensions for more than 9,000 workers and their families—the 1989 collective bargaining agreement, the 1989 employee-shareholder vote for an initial public stock offering, the 1994 collective bargaining agreement and an employee-owner decision in favor of a limited second public stock offering, and the 1997 and 2000 collective bargaining agreements.

By 1989 Weirton Steel confronted a situation in which it had to repurchase Weirton Steel stock shares from retiring steelworkers or permit these retirees to sell their shares publicly.63 Because the company lacked cash with which to repurchase retirees’ shares and finance capital projects, Weirton ESOP managers proposed a public stock sale. The worker-owners agreed to sell four million shares of stock publicly and to permit employees to sell a portion of their holdings. The workers approved the stock offering after safeguarding their control of the company and

retaining 77 percent of the total stock. This offering netted the company approximately US$60 million and enabled it to finance much of its capital improvements program through borrowing. 64

The 1989 collective bargaining agreement restored the concessions that the ISU granted to finance the employee purchase in 1983. From 1989 through 1991, steelworkers received wage increases that restored the wage reductions they incurred during the initial collective bargaining agreement. Rank-and-file members of the Independent Steelworkers Union approved the contract by a vote of 2,692 in favor to 2,505 opposed.65 The close vote reflected ongoing concerns about modernizing the mill to increase productivity, which in turn decreased employment. In addition to wage increases workers regained some vacation and holiday pay.

Because it borrowed heavily to finance its modernization, Weirton Steel owed nearly one-half billion dollars in debts by 1994. Workers confronted a series of difficult choices about eliminating jobs, paying company debt, and protecting their pensions and wages via employee ownership. Weirton workers responded to these pressures by voting as company owners to a limited second public stock sale and by voting as union members for an enhanced early retirement plan that boosted pensions. The early retirement plan enabled company managers to reduce

employment through attrition rather than furloughs. 66

Facing extraordinary pressure to increase productivity and lower costs, Weirton Steel planned to eliminate 25 percent of its remaining 6,800 employees between 1993 and 1995. Having retained majority employee control, workers developed an early retirement plan that added five years of service to every employee’s record and enabled several hundred employees to qualify for Rule of

70/80 pensions. Although the reductions were not attributable to mill or shop closures, the ISU negotiated a pension supplement for steelworkers who voluntarily retired. These steelworkers received a US$700 monthly pension supplement until they reach aged 62 plus a pension increase of approximately US$200–300 per month. This latter increase resulted from the five years of

service credited to eligible employees. Workers approved the early retirement program by a vote of 3,657 to 1,237. 67

The 1993 to 1995 period proved a critical time for Weirton Steel. Although many employees had qualified for pensions several thousand had not qualified. By this time the United States financial community had become deeply critical of Weirton Steel’s supposedly ‘pro-labor’ practices and openly charged that owner-managers ran the company for the benefit of steelworkers and not on behalf of both employee and public shareholders.68 These criticisms ignore the balance that workers needed not only to preserve Rule of 70/80 pensions but also to finance the early retirement program that encouraged older workers to retire early so that younger workers could remain on the job. Had workers permitted an initial proposal for a 1994 stock sale

they would have lost control of the company because they would no longer have owned a majority of shares.69 This loss of control would have jeopardized their defined benefit pensions and left workers with little influence over workforce restructuring. Because workers had to retain controlling ownership in order to enhance pensions and sustain jobs they limited the second stock sale in 1994. Had workers not sustained majority ownership, Weirton’s managers might not have proposed an early retirement plan that in turn permitted younger workers to continue employment and qualify for their pensions. Instead Weirton’s managers, who would have been accountable to outside shareholders, could have proceeded with a mass and permanent layoff of approximately 1,700 steelworkers. Because layoffs proceeded from least to greatest seniority, these 1,700 workers would have lost their jobs before qualifying for Rule of 70/80 pensions.

Recognizing their dilemma that funding better wages and benefits implied or necessitated ceding company ownership, the Independent Steelworkers Union stewards and officers shifted their focus from recouping wages to job preservation. Their 1994 collective bargaining agreement provided annual bonus payments in lieu of permanent wage increases. More importantly, the agreement included a no-layoff clause, automatic recalls of laid-off workers, and protections against company ‘outsourcing’ or using outside labor to perform work that steelworkers could

perform. 70 All of these provisions helped workers qualify for their pensions. ISU rank and file approved this contract by a vote of 2,699 to 1,525.

For the duration of Weirton Steel’s existence it did not make annual operating profits, as it encountered increased competition from both US mini-mill steel manufacturers and foreign imports. The Weirton ESOP continued funding the employees’ defined benefit pension plan and health and life insurance benefits for retirees. In their 1997 collective bargaining agreement Weirton steelworkers received hourly wage increases totaling US$2.50 over three years in the contract. Workers regulated further workforce reductions by adopting annual employment targets.

These targets limited job eliminations to 12 percent of the 4,000 hourly workers who remained. The contract provided that company projects costing less than US$1 million would be performed by ISU labor and 350 workers who voluntarily retired before age 62 would receive severance bonuses of US$7,500 each. 71

As the United States economy entered recession in 2001 Weirton Steel had no options left with which to reduce costs or raise capital. Following the 1989 and 1994 stock issues employees had ceded ownership but retained effective voting control of the company because of provisions that granted disproportionate votes to employee owned stock. In early 2003 Weirton entered bankruptcy, and the company froze its pension plan, thus ending nearly twenty years of contributions to workers’ retirement security.

Analysis of Weirton’s Experience

In 1983 Weirton steelworkers voted for concessions totaling approximately US$193 million over five years in exchange for ownership and opportunities to live and work in their Ohio Valley community. Twenty years later their experiment with employee ownership staggered to its conclusion with the company bankrupt, the United States government taking over pension payments, and a federal bankruptcy judge canceling retirees’ health insurance.72 On its face employee ownership could be deemed a failure. But such an analysis fails to evaluate the twenty years during which the employee-owned Weirton Steel provided pension, health, and life insurance benefits to workers and retirees and it fails to include the value of the insured pension plan. The employee-owned Weirton Steel was neither a citadel of workplace democracy nor a systematic victory for capitalist interests. It was more akin to a two-decade-long high wire act in which employees made important collective decisions about how to retain sufficient control of their company such that they could create the income security that they had sought in the early 1980s.

From 1984 through 2003, Weirton Steel’s pension and retirement payments exceeded the concessions workers made to purchase the plant from 1984 through 1989. The pension fund provided approximately US$400 million in pension benefits and the company paid over US$175 million in health insurance benefits for retirees through 2003 (both figures are in constant 1983 dollars).73 In comparison with the US$193 million in concession provided by the 1983 collective bargaining agreement, Weirton employee-owners provided at least US$575 million in retiree benefits. When the company entered bankruptcy the federal government guaranteed pension payments with a present value of US$1.3 billion (US$722 million in constant 1983 dollars). By adding the retirement benefit payments and the insured value of the pension plan, one can estimate that workers funded benefits worth approximately US$1.3 billion (in 1983 dollars) in exchange for their US$193 million investment. Had the workers invested their US$193 million concessions as a lump sum in January 1984, they would have needed an annual real rate of return of 10.6 percent in order to realize US$1.3 billion in asset value by 2003. 74

The 1994 early retirement plan brings into relief the long-term balance workers sustained. Workers who voluntarily retired early faced lower wages in the local job market where Weirton Steel remained the best-paying employer, and these workers’ pensions were lower than if they had remained working at Weirton Steel until normal retirement age. However, if several hundred workers had not retired then an equal number would have likely been furloughed to reduce Weirton Steel’s operating costs. These younger workers would not have qualified for Rule of 70/80 pensions and would have experienced both lower working wages and lower pensions that would have started at later dates. By enhancing pensions the Weirton ESOP motivated approximately 1,500 workers to retire early, which in turn permitted younger workers to continue working and then qualify for their pensions. The added cost of the US$700 monthly supplement was US$14.3 million annually.

The ESOP campaign focused workers on job and pension security, and pro-ESOP labor leaders had argued that employee ownership provided the means to offset the labor’s concessions. Some of these financial offsets, such as profit-sharing, were direct and can be easily estimated. From 1984 through 1989, the Weirton ESOP distributed US$172 million in profit-sharing bonuses to employees. This compensation offset 89 percent of the value of concessions granted in the 1983 collective bargaining agreement. 75

By far the most important and interrelated factors that contributed to workers’ economic security were maintaining the plant’s integrated steel manufacturing process and retaining its defined benefit pension plan. These two factors reinforced each other. Managers agreed to workforce reductions through attrition rather than department and mill shutdowns. Because department and mill shutdowns would have triggered Rule of 70/80 benefits and corresponding company liabilities such actions would have accelerated Weirton Steel’s financial erosion. Consequently,

neither labor nor management raised the possibility of dramatically altering the steelworks’ steel-making processes, which would have triggered Rule of 70/80 benefits.

In order to sustain employment and help workers qualify for pensions Weirton Steel maintained its integrated steel-making process and made that process increasingly efficient. An alternative strategy would have been to reconfigure the steel-making process from an integrated to a mini-mill process and to shut down large parts of the plant. Weirton’s decision to maintain its steel-making processes provided for gradual reductions in the labor force from voluntary retirements. As one retired union leader John Balzano explained,

We always stressed that we would keep this an integrated mill as long as there were ISU rank and file who came in under [sic] the ESOP and we would keep it that way until everyone qualified under 70/80 . . . If we ever had a major shutdown it would leave us in the hole but we also knew we needed to cut man hours (per ton of steel produced) down over time. So we had to have some balance of producing more with less workers but not getting rid of too many workers too fast because if you do that then you have a whole new problem called ‘I’m broke ’cause everybody got laid off.’ Really, management never raised the issue of not having an integrated works here . . . The idea was if you keep it integrated you keep people working; if you keep people working, you keep the money flowing (into) the pension fund. Then when we get that all taken care of by 70/80, we can talk about taking this down to a mini-mill. 76

In addition to explaining Weirton’s balance between productivity increases and avoiding Rule of 70/80 Balzano’s comments bring into relief how Weirton’s managers and ISU leaders sustained support for the ESOP and even created support for diluting employee ownership when the company needed capital financing in the 1990s. In the 1980s, ISU leaders created a collective interest in keeping jobs and funding pensions. Although not without flaws or limits, this interest remained viable through the company’s existence.

Records from collective bargaining agreements support union leaders’ contentions about job security and pension goals.77 Although the Pension Benefit Guaranty Corporation declared Weirton Steel’s pension plan under-funded, declining investment values, and not excessive benefits, were responsible for the deficit. The loss of asset value became widely prevalent among pension funds in the United States in 2001 through 2003. As late as 2000, Weirton Steel’s pension plan posted a US$90 million surplus and in 2001 its deficit had been a modest US$29 million.78 Although workers lost health and life insurance coverage ERISA protections insured workers pensions up to a maximum of US$43,000 annually. Most ISU retiree pensions ranged

from US$20,000 to US$35,000 annually. Had workers not sustained their defined benefit pension plan and transitioned to individual defined contribution plans, as steelworkers at Geneva Steel and other companies had done, they might have experienced losses averaging 40 percent of their individual pension assets. Compared with Geneva Steel workers, Weirton’s workers created greater economic security and channeled greater wealth to labor than their counterparts.

Conclusion

To conclude I return to the three lessons posed at the beginning. First, although labor progressives did not prevail in creating a day-to-day workplace democracy they played a critical role in the ESOP’s institutional development. Labor progressives motivated the ISU to enfranchise laid-off workers and they credibly threatened the success of the ESOP campaign. Because the ESOP was less costly than alternatives and provided National Steel its best option to avoid shutdown charges, moderate ISU and Joint Study Committee leaders used the tension created by labor progressives’ threat to the ESOP to motivate National Steel to concede its lock-and-freeze pension plan in favor of the work-to-get proposal. Had this political tension not existed ISU leaders

might have recommended settling for a less valuable proposal such as the lock-and-freeze pension plan or even a defined contribution plan.

Second, although workers did not collectively and democratically manage the company on a day-to-day basis, critical democratic votes enabled workers to recoup their concessions, maintain employee ownership and control of the company’s stock, and sustain its pension plan. There were series of votes in 1993 and 1994 that first denied company managers the opportunity to issue more stock and then limited stock to 20 percent of the company’s equity. These votes along with workers’ approval of the early retirement incentives in 1994 and 1997 demonstrated workers’

balance between sustaining jobs and pensions and sustaining the company itself. As former ISU steward Ron Dunn reflected,

Every time we’ve had a vote, it’s been tough. It’s usually a choice between bad and terrible, but we’ve bitten the bullet . . . We’ve made the tough choices to keep the company going, keep as many jobs as possible, and keep the pension checks out there [in the community].

Perhaps the most important lesson reflected in Weirton’s experience is that the workers’ collective action and labor leaders’ ability to create shared interests among old and young workers enabled workers to create more income and greater income security than if they had acted individually. In order to collect Rule of 70/80 pensions, workers had to sustain their defined benefit pension plan. By sustaining Rule of 70/80 pensions, Weirton workers provided economic security for older workers. By extending layoff recalls, sharing in wage concessions, and agreeing to

dilute and eventually yield ownership, younger workers sustained pension funding and benefits for their predecessors and themselves. Had these workers changed their priorities they might have curtailed retirement benefits, particularly retiree health insurance, in order to improve their company’s value during the 1990s.

As a model for community economic investment the Weirton Steel ESOP provides a foundation, albeit not a flawless one, from which community leaders can engage workers to sustain employment and income. Workers provided concessions that financed the capital that sustained their jobs. They demonstrated their ability to balance those jobs with capital improvements and with their collective desire for secure retirements. However, many Weirton community members, from labor and management, found it ironic that although their mill had survived for twenty years, their community had continued a steady economic decline and population losses. Many Weirtonians reflected that although the ESOP had been essential, it had demanded so much community attention and so many resources that other economic development opportunities had been forgone. To improve on Weirton as a model for worker investment it would be worth considering how workers could diversify their interests from a single company to a more community-wide approach. Steelworkers and community members most frequently identified a lack of

economic diversification as the ESOP’s downside. These individuals lamented that in the twenty years during which the ESOP provided economic stability the community focus on steel and steelworkers constrained economic diversification.79 People in the mill and the larger community felt that they should have better balanced sustaining the steel plant and generating new community investments.

In evaluating Weirton steelworkers’ outcomes three counterfactual questions can be posed: (1) What if there had been no legacy costs? (2) What if there had not been the political triangulation created by labor progressives, the ISU, and National Steel’s management? (3) What if Weirton had been sold to private outside investors and not its employees?

In response to the first question, legacy costs motivated National Steel to offer an alternative other than a plant closure and that alternative became the means by which workers sustained their jobs for twenty years. In other steel communities where labor represented fewer workers or companies had already borne the majority of the legacy costs associated with a particular plant, steel manufacturers were decidedly less willing to negotiate alternatives to plant closures. US Steel declined to negotiate with USWA Local 2701 for an employee purchase of the Geneva works and Bethlehem Steel closed its Johnstown works when USWA locals rejected concessions demanded by potential buyers of the Johnstown mills.

Had labor progressives not campaigned against the ESOP it is difficult to know whether the ISU leadership and the Joint Study Committee (JSC) would have negotiated the work-to-get provision that improved the economic value of pension benefits. Considering that the other ESOP opponents were retired and nearly retired workers who were better served by the status quo than the ESOP, it is fair to ascribe the work-to-get and five-year failsafe provisions to the ISU leadership’s political decision to attract support from younger and middle-aged steelworkers. Possibly the ISU would have sought and National Steel’s management would have agreed to work-to-get without the Rank and File Committee’s threat to the ESOP but there would have been less political motivation to do so. In creating a majority coalition, Bish and the ISU stewards reached out to older steelworkers with the five-year failsafe and to younger and middle-aged workers with the work-to-get proposal. In the absence of the Rank and File Committee, the major opposition to the ESOP would have been from older and retired workers. Bish and the JSC appealed to this group with the five-year failsafe, but the larger economic benefits came from the work-to-get proposal that appealed to younger workers.

If private outside investors instead of the employees had purchased the Weirton plant, these stockholders very likely would have responded to the financial crisis of 1993 through 1995 differently than the Weirton steelworkers did. Rather than ceding ownership private investors would have had the option to furlough relatively junior employees. Exercising this option would have lowered labor costs for the plant and would not have created a costly early retirement program. Outside investors could have constrained future pension costs by dismissing employees who had not yet qualified for Rule of 70/80 pensions under the work-to-get provisions of the 1984 ESOP agreement.

Weirton’s experience demonstrates workers’ abilities to respond effectively to long-term economic challenges. Workers confronted challenges in their industry and provided defined benefit pensions and health insurance when many United States firms reduced such benefits. Strategic decisions about employee ownership and income security were made democratically and reflected workers’ understanding of how best to balance company ownership with workers’ and retirees’ incomes. But the larger lesson from the Weirton experiences is that Weirton’s workers created their economic power through their collective, and not individual, bargaining agreements that preceded the ESOP.80 Because dismissing thousands of workers would have cost

National Steel hundreds of millions of dollars, its managers sought an alternative solution and Weirton’s workers used their collective employment contract as a means of creating a new collective financial institution. Although the Weirton ESOP eventually failed, it engaged a process that provided income security and sustained a community’s mainstay employer when many other communities faced more discouraging outcomes.

Acknowledgement

The author wishes to thank Joshua H. Orr for research assistance on this article.

Notes

[1] Strohmeyer, Crisis in Bethlehem, 120–28; Hoerr, And the Wolf Finally Came, 215–24.

[2] Serrin, William, ‘Town Backs Workers in Plan to Buy Steel Mill,’ A16.

[3] Varano, Forced Choices, 79–142.

[4] Bohner, ‘Will Workers Fire Workers?’ 16.

[5] Interviews were conducted between 1997 and 2001 with former and current managers,

Independent Steelworkers Union members, and community members.

[6] Portz, The Politics of Plant Closings, 13–23.

[7] Although US federal law insured defined benefit pensions, most workers had not qualified

for their pensions and thus could not claim any vested benefits until age 65. The Weirton

plant’s ongoing operations permitted workers to qualify as early as age 48 for their pensions.

[8] Imbroscio et al., ‘Local Policy Responses to Globalization,’ 31–32; Wills, ‘A Stake in Place,’

80–82.

[9] Jones and Bachelor, The Sustaining Hand, 3–20.

[10] Weirton steelworkers were not affiliated with the USWA, but their collective bargaining

agreements paralleled those of the USWA and large steel manufacturing firms.

[11] Beamer and Lewis, ‘The Irrational Escalation of Commitment,’ 681–82.

[12] Barber and Rifkin, The North Will Rise Again, 83; Beamer and Lewis, ‘The Irrational

Escalation of Commitment,’ 678–79.

[13] Kelly and Zoric. ‘Lone Wolf at Weirton,’ 444–56.

[14] Lieber, Friendly Takeover, 30–34.

[15] Serrin, ‘Struggling to Save the Local Mill,’ 1.

[16] Wiggins, ‘Workers May Get Weirton Steel Unit,’ D5; Washington Post, ‘Weirton Sale

Possible,’ C11.

[17] Hoerr, And the Wolf Finally Came, 217.

[18] Darling, ‘The City that Refuses to Die,’ B1.

[19] Lieber, Friendly Takeover, 45; Weirton Steel 1984 Annual Report, 2.

[20] The amounts were calculated using approximated yearly pension and health insurance costs

from the Weirton Steel division of National Steel and by using data from mill closures in the

1970s and steel company financial data.

[21] Beamer and Lewis, ‘The Irrational Escalation of Commitment,’ 683–689.

[22] Thompson, ‘Worker Ownership,’ 21–22; Lieber, Friendly Takeover, 125.

[23] Serrin, ‘Struggling to Save the Local Mill,’ 1.

[24] Interviews, January 2000 and November 1998.

[25] Lieber, Friendly Takeover, 109; Varano, Forced Choices, 86–89; Weirton Steel Company

Transfer Agreement with National Intergroup/National Steel Corporation. Weirton, West

Virginia, 11 January 1984. Weirton Steel Corporation: Summary of Collective Bargaining

Agreement with the Independent Steelworkers Union. Weirton, West Virginia, 1984.

[26] The first option would have required an investment of approximately US$35,000 per active

worker in 1982—an amount few workers had. The second option put those employees with

the greatest seniority at the greatest risk. The third option gave the Joint Study Committee

the most latitude to distribute concessions and craft income and pension security in such a

way that a majority of steelworkers would support an employee purchase.

[27] Olson, ‘Union Experiences withWorker Ownership,’ 6–11; Scherer, ‘Workers to the Rescue,’ 1.

[28] Portz, The Politics of Plant Closings, 54–65.

[29] Interviews with former Weirton Division steelworkers and managers.

[30] Varano, Forced Choices, 94–98.

[31] Ibid., 93–94.

[32] Portz, The Politics of Plant Closings, 107–17.

[33] Varano, Forced Choices, 127–30.

[34] Lieber, Friendly Takeover, 114, 121.

[35] Interview with ISU stewards, January 2000; Lieber, Friendly Takeover, 84.

[36] Lieber, Friendly Takeover, 81; interviews, 1997, 2000.

[37] Serrin, ‘Struggling to Save the Local Mill.’

[38] Interviews, Weirton, West Virginia, 1999, 2000.

[39] At this time retired Bethlehem Steel employees were successfully suing the Bethlehem Steel

Corporation in the US District Court in the case of Eardman et al. v. Bethlehem Steel

Corporation, Employee Welfare Benefit Plans, United States Court for the Western District of

New York 607 F. Supp. 196, US Dist. Lexis 20213, 5 EBC 1985. The District Court ruled that

Bethlehem Steel had contractually obligated itself to maintain health insurance benefits,

without premium contributions from retirees. This litigation was ongoing when the Weirton

ESOP campaign took place. Prior to the US court decision National Steel’s managers had

hoped to relieve themselves of this expense, which was approximately US25 million per year.

[40] Weirton Joint Study Committee, Disclosure Document.

[41] Serrin, ‘Struggling to Save the Local Mill.’

[42] Weirton Steel archives, Pennco Building, Weirton Steel Corporation, 1998.

[43] Interview with Walter Bish, January 2000.

[44] Lavine, A Survey of Weirton Steel Employees.

[45] Varano, Forced Choices, 106–30; interviews with Charles Cronin and John Balzano.

[46] Thompson, ‘Worker Ownership,’ 21–22.

[47] Christian, ‘Ink Needs to Dry Before Geneva Is Officially Sold,’ 1; idem, ‘Negotiations

Continue between Steelworkers and Geneva Buyer,’ 3; idem, ‘Steelworkers Vote, ‘‘Yes’’

BMT,’ 1.

[48] Christian, ‘Workers Can’t Have Job, Reap the Benefits Too,’ 1.

[49] This assumes a 3 percent discount rate and an income stream from pension payments

commencing at retirement and continuing until age 77.

[50] Pension Benefit Guaranty Corporation v. Envirodyne Industries, et al., No. 81 C 7076, United

States District Court for the Northern District of Illinois, 16 November 1988. Other

companies’ attempts to avoid Rule of 70/80 responsibilities fueled the Weirton workers’

suspicions. In the early 1980s union workers at Wisconsin Steel, who were represented by the

Progressive Steelworkers Union, sued the steel-maker’s parent firm, International Harvester,

for having engineered the sale of its steel works to avoid paying Rule of 70/80 benefits to

3,000 steelworkers. The expectation among many Weirton steelworkers was that the Weirton

Steel ESOP would operate as an independent company and National would hold promissory

notes resulting from the employee purchase. If the Weirton Steel ESOP failed to make

repayment then National Steel could have liquidated the ESOP’s pension fund and reclaimed

the Weirton plant’s physical assets to satisfy the debt. Bremer, ‘Wisconsin Steel Trial Tests

Navistar, Pension System,’ 1; Crenshaw, ‘Subsidiary Sale Doesn’t End Pension Liability,’ E3.

[51] Interview, Weirton, West Virginia, January 1998.

[52] Weirton Steel Company Transfer Agreement with National Intergroup/National Steel

Corporation; Behr, ‘Weirton’s Gamble,’ H1.

[53] Behr, ‘Weirton’s Gamble,’ H1; Scherer, ‘Workers to the Rescue,’ 1.

[54] Christian, ‘Steelworkers Vote ‘‘Yes’’ BMT,’ 1.

[55] Author interviews with USWA Local 2701 officers and Geneva Steel manager.

[56] Bar Technologies, Prospectus; interview with Johnstown Area Regional Industries official.

[57] Boselovic, ‘262 Lose Jobs with Johnstown Steel Mill Closing.’

[58] Serrin, ‘Steelworkers Approve Plan to Buy Their Own Plant in West Virginia,’ 9.

[59] New York Times, ‘Weirton Steel Sale Is Backed,’ 30.

[60] Weirton Steel 1984 and 1985 Annual Reports.

[61] Russell, ‘Lessons from the Recent Failure of Weirton Steel’s ESOP.’

[62] Bohner, ‘Will Workers Fire Workers?’ 16.

[63] United States laws governing employee stock ownership plans restricted stock ownership to

active employees and from retired workers.

[64] Scolieri, ‘Weirton Has SEC Nod for Stock Sales.’

[65] Balcerek, ‘Weirton, Hourly Workers in Accord.’

[66] Scolieri, ‘Weirton Union OK’s Revised Pension Plan;’ idem, ‘Weirton Board OK’s Stock

Offering.’

[67] Scolieri, ‘Weirton Union OK’s Revised Pension Plan.’

[68] Scolieri, ‘Weirton Directors Address Stock Offering, Labor Talks;’ Bohner, ‘Will Workers

Fire Workers?’

[69] Scolieri, ‘Weirton Votes Change in Company’s Bylaws.’

[70] Cimini, ‘Weirton Steel Settlement.’

[71] Sacco, ‘Weirton Union Reach Tentative Accord;’ New Steel, ‘Weirton’s New Labor Contract.’

[72] Smith, ‘Judge Ends Health Care Coverage for 9,000 Weirton Steel Retirees.’

[73] Figures are based upon information provided in Weirton Steel Annual Reports, 1984

through 2003.

[74] Author calculation based upon figures adjusted for US inflation and using <http://

cgi.money.cnn.com/tools/returnrate/returnrate.jsp>

[75] Weirton Steel Annual Reports, 1984 through 1989.

[76] Interview with John Balzano, March 2001.

[77] Scolieri, ‘Union Workers OK New Pact at Weirton Steel;’ New Steel, ‘Weirton’s New Labor

Contract.’

[78] Robertson, ‘Weirton Wowed by Pension Performance;’ Boselovic, ‘Steel Pensions OK.’

[79] Interviews, Weirton, West Virginia, 1997 through 2001.

[80] Barber and Rifkin, The North Will Rise Again, 37–43.

References

Balcerek, Tom. ‘Weirton, Hourly Workers in Accord.’ American Metal Market, 98, no. 23

(Feb. 1990).

Bar Technologies. Prospectus. Johnstown, Penn., 1997.

Barber, Randy, and Jeremy Rifkin. The North Will Rise Again: Pensions, Politics, and Power in the

1980s. Boston: Beacon Press, 1978.

Beamer, Glenn, and David E. Lewis. ‘The Irrational Escalation of Commitment and the Ironic

Labor Politics of the Rust Belt.’ Enterprise and Society 4, no. 4 (2003): 676–706.

Behr, Peter. ‘Weirton’s Gamble: Employee Ownership of Plant Poses Risk, Sacrifice, Reward.’

Washington Post, 25 September 1983, H1.

Bohner, Kate. ‘Will Workers Fire Workers?’ Forbes, 19 July 1993, 16.

Boselovic, Len. ‘262 Lose Jobs with Johnstown Steel Mill Closing.’ Pittsburgh Post-Gazette, 7 June

2000, C1.

––––. ‘Steel Pensions OK; Other Benefits Uncertain.’ Pittsburgh Post-Gazette, 24 January 2001, 1.

Bremer, Brian. ‘Wisconsin Steel Trial Tests Navistar, Pension System.’ Crain’s Chicago Business, 21

March 1988, 1.

Christian, Patrick. ‘Ink Needs to Dry Before Geneva Is Officially Sold.’ Daily Herald, 31 May 1987, 1.

––––. ‘Negotiations Continue between Steelworkers and Geneva Buyer.’ Daily Herald, 5 June 1987, 3.

––––. ‘Steelworkers Vote ‘‘Yes’’ BMT.’ Daily Herald, 21 June 1987, 1.

––––. ‘Workers Can’t Have Job, Reap the Benefits Too.’ Daily Herald, 16 June 1987, 1.

Cimini, Michael H. ‘Weirton Steel Settlement.’ Monthly Labor Review, 113, no. 2 (1994).

Crenshaw, Albert B. ‘Subsidiary Sale Doesn’t End Pension Liability.’ Washington Post, 17 November

1988, E3.

Darling, Lynn. ‘The City that Refuses to Die: Weirton Workers Fight for the Best Years of Their

Lives.’ Washington Post, 6 July 1982, B1.

Hoerr, John P. And the Wolf Finally Came: The Decline of the American Steel Industry. Pittsburgh:

University of Pittsburgh Press, 1988.

Imbroscio, David L., Thad Williamson, and Gar Alperovitz. ‘Local Policy Responses to

Globalization: Place-Based Ownership Models of Economic Enterprise.’ Policy Studies

Journal 31, no. 1 (2003): 31–52.

Jones, Bryan D., and Lynn W. Bachelor. The Sustaining Hand: Community Leadership and Corporate

Power. 2nd ed. Lawrence: University Press of Kansas, 1993.

Kelly, Eileen P., and Joseph A. Zoric. ‘Lone Wolf at Weirton: Ernest Tener Weir.’ Journal of

Managerial Issues 6, no. 4 (1994): 444–56.

Lavine, Arnold. A Survey of Weirton Steel Employees on the Eve of Their Historic Vote. Morgantown:

West Virginia University, Department of Sociology, 1983.

Lieber, James B. Friendly Takeover: How an Employee Buyout Saved a Steel Town. New York: Viking

Press, 1995.

New Steel. ‘Weirton’s New Labor Contract: Fewer Jobs but Less Outsourcing.’ 13, no. 4 (1997): 11.

Olson, Debarah Groban. ‘Union Experiences with Worker Ownership: Legal and Practical Issues

Raised by ESOPS, TRASOPS, Stock Purchases, and Co-operatives.’ Wisconsin Law Review,

September/October 1982, 729–808.

Portz, John. The Politics of Plant Closings. Lawrence: University Press of Kansas, 1990.

Robertson, Scott. ‘Weirton Wowed by Pension Performance.’ American Metal Market, 18 February

2000, 5.

Russell, John D. ‘Lessons from the Recent Failure of Weirton Steel’s ESOP.’ Labor Notes, no. 302

(2004):9–11.

Sacco, John E. ‘Weirton Union Reach Tentative Accord; 4½-year Labor Pact Awaits Workers’

Approval.’ American Metal Market, 3 March 1997.

Scherer, Ron. ‘Workers to the Rescue: Can Employee Ownership Keep Factories Open?’ Christian

Science Monitor, 16 November 1982, 1.

Scolieri, Peter. ‘Weirton Has SEC Nod for Stock Sales.’ American Metal Market, 15 June 1989.

––––. ‘Weirton Union OK’s Revised Pension Plan.’ American Metal Market, 11 February 1993.

––––. ‘Weirton Board OK’s Stock Offering.’ American Metal Market, 6 September 1993.

––––. ‘Weirton Directors Address Stock Offering, Labor Talks.’ American Metal Market, 8

December 1993.

––––. ‘Weirton Votes Change in Company’s Bylaws.’ American Metal Market, 18 April 1994.

––––. ‘Union Workers OK New Pact at Weirton Steel.’ American Metal Market, 14 March 1994, 7.

Serrin, William, ‘Town Backs Workers in Plan to Buy Steel Mill.’ New York Times, 8 June 1982,

A16.

––––. ‘Steelworkers Approve Plan to Buy Their Own Plant in West Virginia.’ New York Times, 24

September 1983, 9.

––––. ‘Struggling to Save the Local Mill.’ New York Times, 13 February 1983, Section 3, 1.

Smith, Vicki. ‘Judge Ends Health Care Coverage for 9,000 Weirton Steel Retirees.’ Chicago Sun-

Times, 16 March 2004, 1.

Strohmeyer, John. Crisis in Bethlehem: Big Steel’s Struggle to Survive. Pittsburgh: University of

Pittsburgh Press, 1994.

New York Times. ‘Weirton Steel Sale Is Backed.’ 31 December 1983, 30.

Thompson, Donald B. ‘Worker Ownership: Weirton’s Salvation.’ Industry Week, 5 September 1983,

21–22.

Varano, Charles S. Forced Choices: Class, Community, and Worker Ownership. Albany: State

University Press of New York, 1999.

Washington Post. ‘Weirton Sale Possible.’ 3 March 1982, C11.

Weirton Joint Study Committee. Disclosure Document. Weirton, W.V.: Weirton Steel Corporation,

1983.

Wiggins, Phillip H. ‘Workers May Get Weirton Steel Unit.’ New York Times, 3 March 1982, D5.

Wills, Jane. ‘A Stake in Place: The Geography of Employee Ownership and Its Implication for a

Stakeholding Society.’ Transactions of the Institute of British Geographers, New Series, 23,

no. 1 (1998): 79–94.