Glenn Beamer

Rutgers University

Abstract

This article outlines the work incentives and income support provided by the federal Earned Income Tax Credit (EITC) and illustrates how state earned income and dependent care credits assist working poor families. State earned income and dependent care tax credits serve as critical complements to the EITC, the federal government’s largest antipoverty program. By attending to specific components of each tax credit, state policymakers can maximize state funds that qualify for federal maintenance of effort requirements under the Personal Responsibility and Work Opportunity Reconciliation Act (PROWRA), and they can reinforce positive effects and offset work disincentives stemming from current federal tax parameters.

During the 1990s, federal and state policymakers focused on policies that encouraged work and economic independence among families. In addition to transforming Aid to Families with Dependent Children (AFDC) into Temporary Assistance to Needy Families (TANF), Congress expanded the Earned Income Tax Credit (EITC) in 1990 and 1993. In 2001 Congress expanded the Dependent Care Tax Credit that provides tax relief for child care expenses. In the eight years since Congress passed the Personal Responsibility and Work Opportunity Reconciliation

Act (PROWRA; Pub. L. No. 104–193), more than twenty-five states have followed the federal lead and enacted their own earned income and dependent care tax credits. Seventeen states have earned income tax credits and twenty-seven states provide dependent care credits. The first section of this article reviews the federal EITC and outlines how state credits can reinforce these effects. The second section evaluates state parameters for tax credits as components of welfare reform and estimates state costs of earned income and dependent care credits and offers policy

options for state policymakers that reinforce the positive effects of the federal tax credits or address potential drawbacks.

Although PROWRA did not directly address the EITC, PROWRA’s caseload reduction targets and workforce participation requirements implied that the EITC would become a major component in supporting single parents’ work efforts and in lifting children in working poor families out of poverty. Prior to its last expansion, which became fully effective in 1996, the EITC reduced the poverty rate among single mother households from 42.7% to 40.7%. By 2001, the EITC reduced poverty among single mother households from 30.9% to 26.2%—nearly doubling its antipoverty effectiveness (United States House of Representatives, 2004). Thus,

even in the absence of welfare reform, the federal EITC would have grown as a component in public efforts to encourage work and combat poverty.

Over twenty million families receive EITC benefits annually. In contrast, monthly TANF caseloads average slightly more than five million families. In ten states the EITC assists eight times as many families as TANF income assistance

grants. In twenty-one states, workers earning the minimum wage at full-time, year-round jobs receive EITC benefits that exceed the maximum annual TANF cash allowance in their states. For families with annual wages below $6,000, the EITC increases family income by an average of 30%. For families with incomes ranging from $6,000 to $12,000, the EITC increases income by an average of 25% (United States House of Representatives, 2004).

Earned income and dependent care tax credits provide policy tools that reward work, offset job-related expenses, and increase income. Following passage of the Family Support Act in 1988 (Pub. Law No. 100-485), only one state had an earned income tax credit. Since the passage of PROWRA in 1996, twelve states have

adopted earned income tax credits and twenty states have adopted dependent care tax credits. State tax credits, particularly refundable tax credits, provide targeted and equitable assistance for children in low-income families and support parents’ efforts to attain economic self-sufficiency (Blank, 1997; Ellwood, 2001).

The Federal Earned Income Tax Credit

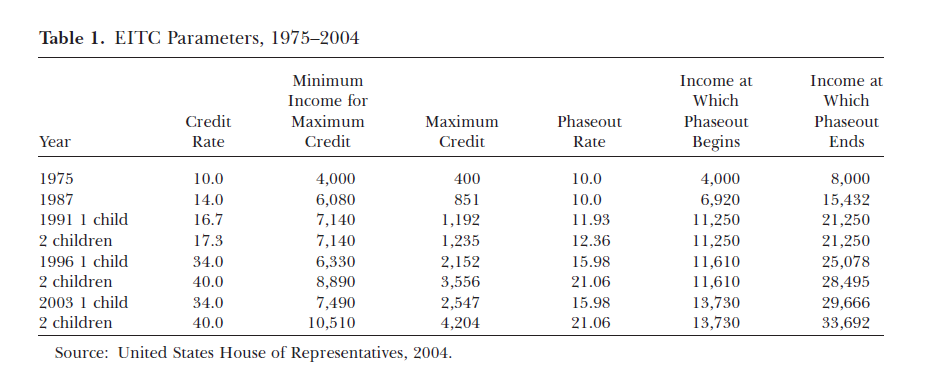

Congress enacted the Earned Income Tax Credit to offset social security taxes for low-income families in 1975. Bipartisan majorities of Congress and Presidents Reagan and Bush supported EITC expansions in 1986 and 1990. In 1993 President Clinton advocated and Congress enacted a major expansion of the EITC that adjusted the credit for family size and provided a small credit for low-income, childless workers (Ventry, 2001). Table 1 provides a history of EITC rates, income thresholds, and eligibility limits.

Upon initial enactment the federal EITC provided modest income tax rebates to low-wage workers with children in an effort to offset regressive payroll taxes. In 1975, 6.2 million families claimed the EITC and the federal government provided $1.25 billion in tax relief, 75% of which took the form of refundable tax credits. Families received an average tax credit of $201 ($708 in 2004 dollars). By 2003, more than 19 million families claimed the EITC. The overall costs of the credit have risen to $34.4 billion, and nearly 90% of the costs are cash refunds to recipients,

while the remaining 10% represents reduced tax payments. The average EITC credit among households with children is $1,784.

Approximately half of the growth in federal assistance to working poor families during the 1990s can be attributed to the EITC (Ellwood, 2001). Since the 1980s, the EITC has become a critical component in efforts to alleviate poverty among working families and to reduce welfare dependency (Howard, 1997; Ventry, 2001). The expanded EITC provided support for work and income that moved low income families closer to the poverty line.

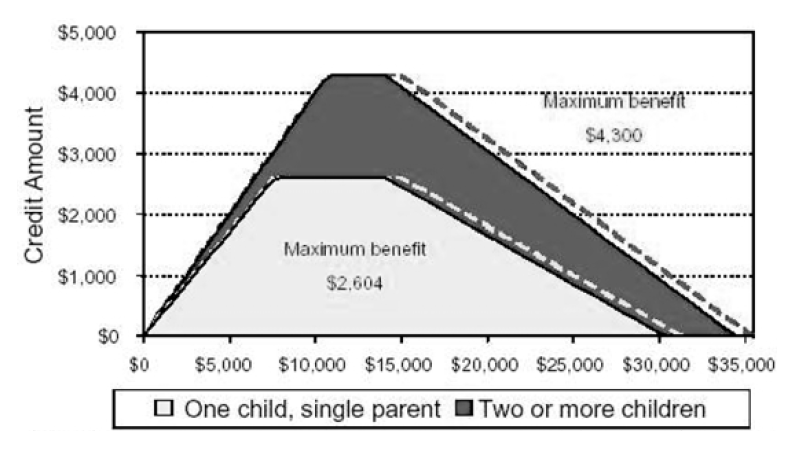

The federal EITC has been expanded to provide a larger credit for families with two or more children. For families with one child, the EITC provides up to $2,547, and for families with two or more children, the EITC provides a maximum benefit of $4,204 annually. The amount of the credit rises along with a family’s wage earnings until wages reach $7,490 for families with one child and $10,750 for families with two or more children. For families with incomes in excess of $13,730, the EITC declines by sixteen cents and twenty-one cents per dollar of additional earnings for

families with one child, and two or more children, respectively. The EITC phases out completely for families with incomes above $33,692. Figure One illustrates the EITC’s parameters.

The federal EITC has become a critical and substantial component in policymakers’ efforts to “make work pay.” The 1990 and 1993 EITC expansions effectively reversed work disincentives and constraints on family income for working poor families (Ellwood, 2000, 2001; Meyer & Rosenbaum, 2001). In the mid-1980s, a single mother with two children was likely to have more disposable income if she remained out of the workforce and relied on AFDC payments and food stamps for her income than if she entered the work force (Blank, 1997; Danziger & Beamer,

1995; Ellwood, 2001).

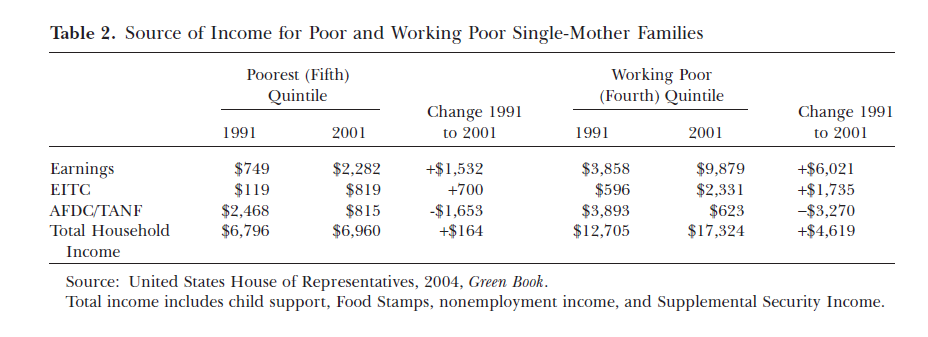

Studies of single mothers’ incomes reflect the growing role of EITC in combating poverty and in economically sustaining working poor families. In 1987, the EITC provided $108 of $7,051 (in constant 2001 dollars) in annual income among women in the bottom quintile of single-mother families. In contrast, AFDC and General Assistance provided families in this quintile with an average benefit of $2,912 annually. By 1996, the mean EITC benefit among single-mother households in the bottom quintile had risen to $563 per year, and AFDC benefits had dropped to a mean of $2,168 per household. By 2001, the mean EITC benefit had increased to $819 per household and represented nearly 12% of the mean household’s net income of $6,960 (United States House of Representatives, 2004).

Among working poor single-mother households, the importance of the EITC has been even more pronounced for families in the fourth lowest quintile of singlemother headed households. In 1987, earnings among the fourth quintile of singlemother households averaged $3,654, EITC benefits averaged $403, and net family income was $13,052 per year (in 2001 dollars). By 2001, earnings among this quintile had risen to $9,879 annually, and the EITC had risen to a mean of $2,331. Of the $1,928 increase in EITC benefits, $685 resulted from increased earnings and

$1,243 can be attributed to the increased credit rates, including the higher rate for families with two or more children. Over this same period, cash welfare benefits from AFDC, and then TANF, declined from $4,517 in 1987 to just $623 by 2001 (United States House of Representatives, 2004).

For both the fourth and fifth quintiles of single-mother families, the EITC grew as a component of household income during the 1990s. For families in the lowest quintile, EITC benefits grew seven-fold from $119 in 1991 to $819 in 2001. This increase offset much of the $1,653 average decrease in AFDC (later TANF) benefits during the decade and enabled single-parent families at the bottom of the income distribution to sustain average household income during the 1990s. In the absence of the 1990 and 1993 EITC expansions, these families would have experienced

approximately a $200 decrease, instead of a $200 increase, in their average annual incomes.

For working poor single-mother families, those in the fourth quintile, the federal EITC was even more beneficial. Substantially higher earnings combined with increased EITC rates enabled these families to experience a 36% average net increase in household income of $4,619. Increases in earnings and EITC benefits more than offset drastic decreases in cash transfer payments. In the absence of the earnings and EITC increases, families in the fourth quintile would have experienced a $3,270 decrease in average annual household income (United States House

of Representatives, 2004). Table 2 summarizes average annual incomes and its sources among poor and working poor single-mother families.

Any equation designed to end welfare dependency, encourage work, and reduce poverty incorporated EITC participation and benefits. For families seeking to leave welfare, EITC benefits typically equal or exceed their previous TANF benefits and comprise approximately 20% to 30% of their disposable incomes (Ellwood, 1999; Greenberger & Anselmi, 2003; Blank, 1997; Meyer & Rosenbaum, 2001). For single-parent families in which the family head faced low-wage employment, the EITC boosted earnings by 14% in the 1980s and this figure rose to as much as 40%

by the time the 1993 expansion became complete in 1996.

The major policy drawback created by the EITC concerns its phase-out range and the implicit marginal tax rates workers face as their wages rise from seven to fifteen dollars per hour. Studies have consistently shown that the EITC provides substantial work incentives, especially for single parents enrolled in cash assistance programs such as TANF and the former AFDC (Ellwood, 2001; Meyer & Rosenbaum, 2001a, b). Ellwood (2001) and Meyer and Rosenbaum (2001b) credit the EITC as the primary force behind the increased labor force participation among single women with children from 62% to 81% and with substantially decreasing the differential labor force participation among married and unmarried mothers.

A concern about the federal EITC has been that many families receive the entire payment in a single lump sum when they file their federal tax returns. In response to this concern, Congress changed the EITC in 1996 to allow for a portion of it to be paid to eligible workers throughout the year. Studies of families’ uses for the EITC reveal that the single payment does not lead to impulsive or frivolous spending. Smeeding, Phillips, and O’Connor (2001) studied families who received the EITC in 1997. Eighty-three percent of families surveyed used a portion of their

credits to pay outstanding bills, 74% purchased cars or other durable goods, and 50% of all recipients reported using their EITC for savings. Sixteen percent of families benefiting from the EITC planned to use it for tuition and job training and 20% planned expenditures that would enable them to remain in or reenter the work force (Smeeding et al., 2001, p. 1198). These latter uses reflect commitments to economic mobility and demonstrate families’ willingness to invest their EITC benefits in ways that provide greater economic security or opportunity. In comparison

to the current TANF program, EITC rebates help four times as many families and establish an income floor for families in all states.

Prior to the 1990 EITC expansion, only one state had an earned income tax credit. Currently, seventeen states and the District of Columbia augment the federal EITC with their own earned income tax credits. Child care credits have become even more prevalent, with twenty-seven states adopting them since the passage of PROWRA. The next section reviews the designs of these state policies. It outlines the range of state assistance provided via tax credits and identifies policy issues state policymakers have engaged.

State Tax Credits

State tax credits provide state welfare administrators with tools by which to move families from welfare dependence to economic independence. Although state earned income tax credits are unlikely to alleviate poverty to the extent the federal EITC does, states can structure their tax credits to offset costs associated with working and to augment federal antipoverty efforts (Cauthen, 2002; Greenberger & Anselmi, 2003; Zahradnik & Llobrera, 2004). The PROWRA provides that states may count funds expended for refundable portions of state earned income and

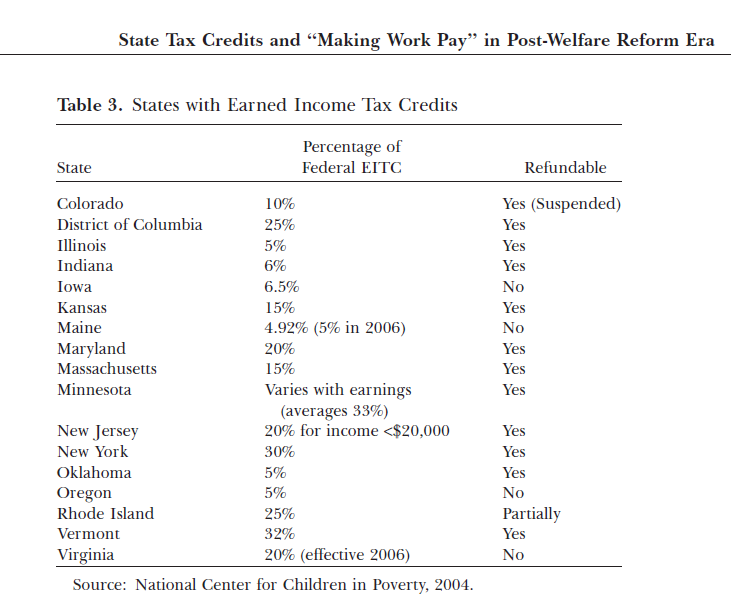

dependent care credits toward their TANF maintenance of effort requirement. The maintenance of effort requirement provides that states must continue to spend 80% of the amount they spent on AFDC in 1994. The allowance to count tax refunds gives states incentives to shift to state tax expenditures as components of their welfare reform strategies. Seventeen states and the District of Columbia have enacted earned income tax credits. Among these states, eleven, and Washington, DC, have implemented refundable tax credits and six have nonrefundable

tax credits.

Refundable credits provide reductions in income tax liabilities for families who qualify for the federal EITC and cash rebates for amounts beyond state tax liabilities. In states with nonrefundable tax credits, families receive tax credits up to the amount of their state income tax liabilities. States adopting refundable EITCs can use funds expended for cash rebates as part of their 80% maintenance of effort required by PROWRA. This provision allows states to support work and fight poverty by shifting funds from TANF cash assistance to their state tax credits.

State earned income tax credits can enhance work incentives, especially for single parents entering the work force. State EITCs offset the costs of entering the labor force by reducing a family head’s state tax liability and by providing cash income in states with refundable credits. Among the states with programs currently, New York’s EITC provides families with cash rebates of up to $1,290 annually. At the other end of the spectrum, Iowa’s EITC offsets family tax burdens by a maximum of $252. In terms of improving family well-being, state EITCs increase

family income-to-needs ratios by a minimum of 0.2% in Maine to a maximum of 9% in Minnesota (National Center for Children in Poverty, 2001). Among states with nonrefundable credits, increases in income-to-needs ratios range from 0.2% to 1.4%. Among states with refundable state tax credits, these increases range from 1.4% in Indiana to 9.0% in Minnesota (National Center for Children in Poverty, 2001).

In the overwhelming majority of states with earned income tax credits, state tax credits are calculated as a proportion of an eligible family’s federal earned income tax credit. This design has made state EITC administration straightforward for families and state administrators. Kansas, for example, has a refundable credit in which a family’s state EITC is 10% of its federal EITC. A Kansas family eligible to receive the maximum $3,888 federal EITC would receive a tax credit of $388 with any portion above its state income tax liability being refundable. In Iowa, which has a nonrefundable credit pegged at 6.5% of the federal EITC, a family could receive a maximum state benefit of $252 or it could eliminate its income tax liability. Table 3 lists states with earned income tax credits and indicates whether the credit is refundable and the size of the credit relative to the federal EITC.

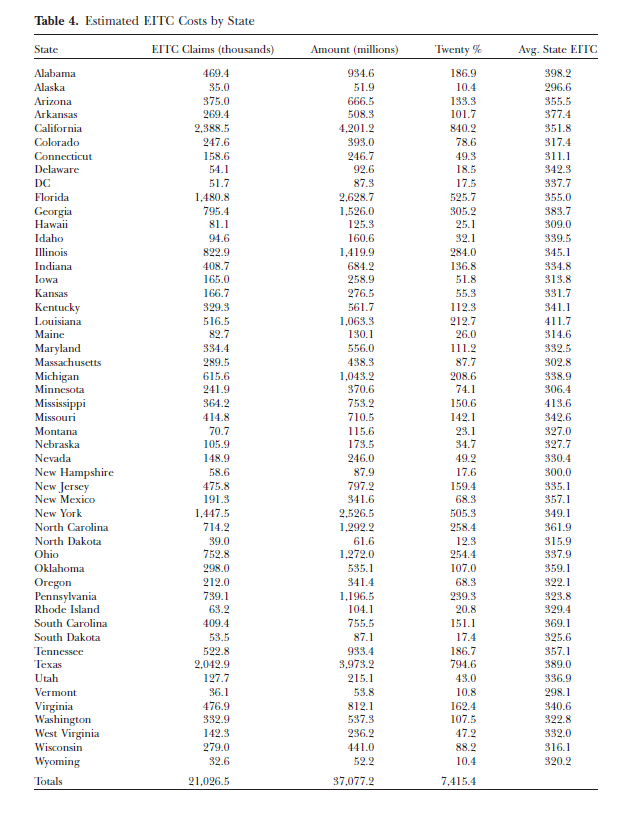

Considering the substantial diffusion of state income tax credits, a reasonable question is how much a complementary state EITC would cost if all fifty states chose to adopt a similar credit. Table 4 provides estimates of the costs of enacting state earned income tax credits across all fifty states. Although nine states do not impose income taxes, these states could structure state rebate programs to offset sales and excise taxes that tend to be regressive and most affect low-income families.

If all states adopted an EITC based on the federal Earned Income Tax Credit, low-income families would receive approximately seven billion dollars in income assistance, with benefits for individual families in the range of three to four hundred dollars. Of course, the costs to individual states would vary based on labor force participation, job availability, and wage and income distribution. Notably, two states without state income taxes, Florida and Texas, would be states providing relatively large proportions of their populations with state EITC benefits. Nearly

20% of the seven billion dollars in annual costs would occur in Florida and Texas. Although these states lack income tax systems, policymakers could design tax credits that offset the relatively high and broad-based sales taxes in those states and thus achieve several of the same policy goals of the income tax rebates.

Thus far state EITC adoptions have taken place mostly in the Northeast and Midwestern states. Virginia recently enacted an EITC as part of its 2004 tax reform package, thus making it the first southern state to move toward increased support for work through its tax code (Llobrera & Zahradnik, 2004). Among states with earned income tax credits, child poverty rates average 17.4% compared to an average child poverty rate of 19.1% in states without earned income tax credits.

The downside of “piggybacking” state earned income tax credits on the federal EITC structure is that state credits may compound work disincentives in the phaseout range of the federal EITC. However, Minnesota’s redesign of its EITC demonstrates that state tax credits can be configured to complement the positive incentives from the federal EITC and to offset work disincentives that may emerge as family incomes increase into the phase-out range of the federal credit (Greenberger & Anselmi, 2003; Manzi & Michael, 2004).

Minnesota has modified its original EITC to address some of the policy concerns that have been raised about the federal EITC. In order to avoid compounding any

work disincentives for married couples whose income fall in the phase-out range of the federal EITC, Minnesota legislators shifted from a state EITC based on the federal EITC to a tax credit, the Minnesota Working Families Credit, that is based on earnings. Like the federal credit, the Minnesota credit grows with income up to a plateau and then remains level until income exceeds $13,000. However, the Minnesota credit now adds a credit “bubble” that coincides with the initial phase-

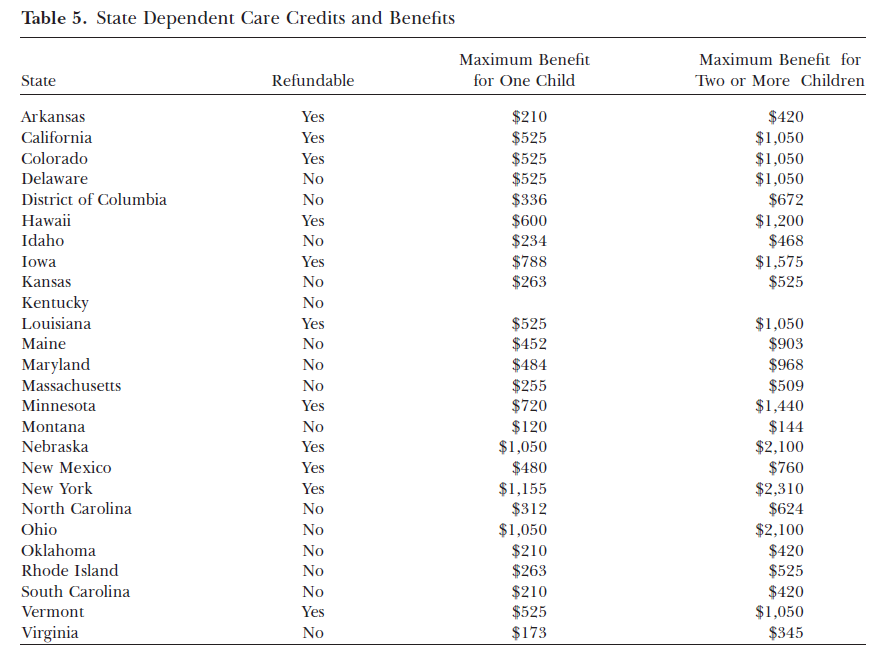

out of the federal credit and provides families with an additional $200 in income assistance that offsets a portion of the declining federal EITC (Greenberger & Anselmi, 2003; Manzi & Michael, 2004). While state earned income tax credits provide relief from state income taxes and, in states with refundable credits, additional disposable family income, some state policymakers have perceived a need to target specific costs associated with leaving welfare and returning to the work force. State dependent care credits, which offset child care costs, provide a means of assisting families in achieving economic self-sufficiency and remaining in the work force (Table 5).

Dependent and Child Care Credits

Dependent and child care tax credits work much like the EITC except that these credits offset documented child care expenses for families transitioning from welfare to work. The federal credit provides that families may reduce their federal income tax liability by 20% of their child care expenses up to a maximum of $1,050 for one child and $2,100 for two children. The vast majority of state credits are calculated as a percentage of the federal credit. Of the twenty-seven states that have dependent or child care credits, twelve provide for refundable credits and fifteen provide nonrefundable credits. The states with nonrefundable credits limit both the positive work incentives and income assistance from their credits to the tax liabilities for working poor families (Greenberger & Anselmi, 2003; National Center for Children in Poverty, 2004). Table 5 lists states with dependent care credits, their maximum levels of assistance, and indicates whether the credit is refundable.

The extent to which refundable child care credits would further facilitate welfare to work is an open question. Among the poorest fifth of single-mother families, the percent of families with one or more earners has increased from 38.9% in 1995 to 69%. Among all single-mother families, this proportion has increased from 73.6% to 89.2% over the same period. However, only 11.2% of the poorest families and 18.9% of all single-mother families report child care expenses (United States House of Representatives, 2004). These low percentages may indicate that single mothers

rely on relatives and friends to provide child care when they work, and introducing child care subsidies might motivate some single parents to move their children into formal care arrangements. However, the low rates of child care utilization indicate that refundable child care credits may assist far fewer families than earned income credits. The latter credits provide assistance based solely on income and not on spending, and thus provide families with financial discretion.

Unlike state earned income tax credits, which complement the federal refundable EITC, refundable state dependent care credits fill a gap created by the nonrefundable federal dependent care credit. Because the federal credit is nonrefundable and because the federal EITC lowers federal tax liabilities for working poor families, state efforts to provide tax subsidies for child care for the working poor can become the largest source of assistance for families transitioning from welfare to work.

By using state tax systems to support work and raise incomes, state policymakers can take advantage of administrative and policy advantages. Because state EITCs and dependent care credits are in the tax system, and not the welfare system, the benefits avoid the stigma associated with traditional welfare programs and thus may encourage higher participation. Second, states can target the benefits to focus assistance on particular groups, such as those transitioning from complete welfare dependence to economic independence, and policymakers can dovetail tax benefits with the parameters of their TANF and other work force development programs. Third, because wages trigger benefits, program administrators need not monitor beneficiaries for time limits.

The disadvantages of tax benefits as components in welfare to work strategy are most evident in the nine states that have no state income tax. In these states new administrative structures may be required and state program personnel may find that other programs such as food stamps would better serve beneficiaries. Because these states lack income taxes and low-income families are particularly unlikely to file tax returns, these nine states would have to conduct extensive outreach programs to enact tax rebates against sales and other taxes. This added administrative

burden would likely compound as these states attempt to integrate tax credits with their existing TANF policies for earnings disregards and work support.

The federal EITC has provided state policymakers with an important tool with which to move families from welfare to work. Without the EITC, the elements of the welfare trap that led to long-term dependency on AFDC would remain. Families on TANF would likely find that child care costs, payroll taxes, and job expenses would offset whatever income increases resulted from leaving TANF in favor of work. With the federal EITC and complementary state tax credits, families are more likely to achieve economic self-sufficiency and decrease their

reliance on cash assistance programs like TANF.

About the Author

Glenn Beamer is an Assistant Professor in the Bloustein School of Planning and Public Policy at Rutgers University. His research focuses on policy diffusion among the American states.

He is the author of Creative Politics: Taxes and Public Goods in a Federal System (University of Michigan Press, 1999), and his articles have appeared in the Journal of Health Politics, Policy,

and Law, Enterprise and Society, PS: Political Science & Politics, and State Politics and Policy Quarterly.

References

Blank, R. M. (1997). It takes a nation: A new agenda for fighting poverty. New York: Russell Sage Foundation.

Cauthen, N. K. (2002). Improving children’s economic security: Research findings about increasing family income through

employment. Policy Brief No. 2: Earned Income Tax Credits. New York: National Center for Children in

Poverty.

Danziger, S. H., & Beamer, B. (1995). Children in poverty: Lessons from the economy and public policy. In

R. E. Ratcliff, M. L. Oliver, & T. M. Shapiro (Eds.), Research in politics and society: The politics of wealth and

inequality (Vol. 5). Greenwich, CT: JAI Press.

Ellwood, D. T. (2000). The impact of the Earned Income Tax Credit and social policy reforms on work,

marriage, and living arrangements. National Tax Journal, 53(4), 1063–1105.

———. (2001). The impact of the Earned Income Tax Credit and social policy reforms on work, marriage,

and living arrangements. National Tax Journal, 53(4), 1063–1105.

Greenberger, D., & Anselmi, R. (2003). Making work pay: How to design and implement financial work supports to

improve child well-being and reduce poverty. New York: Manpower Demonstration Research Corporation.

Howard, C. (1997). The hidden welfare state: Tax expenditures and social policy in the United States. Princeton, NJ:

Princeton University Press.

Llobrera, J., & Zahradnik, B. (2004). A hand up: How state earned income tax credits help working families escape

poverty in 2004. Washington, DC: Center for Budget and Policy Priorities.

Manzi, N., & Michael, J. (2004). The federal Earned Income Tax Credit and the Minnesota Working Family Credit.

Information Brief. St. Paul: Minnesota House of Representatives.

Meyer, B. D., & Rosenbaum, D. T. (2001a). Making single mothers work: Recent tax and welfare policy and

its effects. In B. D. Meyer and D. Holtz-Eakin (Eds.), Making work pay: The Earned Income Tax Credit and

its impact on America’s Families. New York: Russell Sage Foundation.

———. (2001b). Welfare, the Earned Income Tax Credit, and the labor supply of single mothers. Quarterly

Journal of Economics, 116(3), 1063–1114.

National Center for Children in Poverty. (2001). Untapped potential: State earned income tax credits and child poverty

reduction. Research Brief No. 3. New York: Author.

———. (2004). Data provided regarding state dependent care tax credits. New York: Author.

Personal Responsibility and Work Opportunity Reconciliation Act of 1996, Pub. L. No. 104–193, 104th Cong.,

2nd Sess. (1996)

Smeeding, T. M., Phillips, K. R., & O’Connor, M. (2001). The EITC: Expectation, knowledge, use, and economic

and social mobility. National Tax Journal, 53(4), 1187–1209.

United States House of Representatives. (2004). Background materials and data on the programs within the jurisdiction

of the Committee on Ways and Means. Washington, DC: Author.

Ventry, D. J., Jr. (2001). The collision of tax and welfare politics: The political history of the Earned Income

Tax Credit. In B. D. Meyer & D. Holtz-Eakin (Eds.), Making work pay: The Earned Income Tax and its impact

on America’s families. New York: Russell Sage Foundation.

Zahradnik, B., & Llobrera, J. (2004). A hand up: how state earned income tax credits help working poor families escape

poverty in 2004. Washington, DC: Center on Budget and Policy Priorities.