Glenn Beamer

University of Maine

During the 1990s, federal and state policymakers focused on policies that encouraged work and assisted families to become economically independent. In 1996 congress passed the watershed Personal Responsibility and Work Opportunity Reconciliation Act (PRWORA), which is typically referred to as welfare reform. After congress enacted this legislation, state legislatures and governors began developing and implementing a wide range of policies designed to raise incomes for working families, provide assistance with health and child care, and ensure that no family with a full-time worker would fall below the poverty line (in 007, this is $ 0,650 for a family of four). Chief among these programs have been state earned income tax credits, which lower tax burdens and raise living standards for families with low-wage workers. Along with the federal earned income tax credit (EITC ), states and the District of Columbia have focused tax relief, provided work incentives, and raised living standards by relying upon state earned income tax credits.

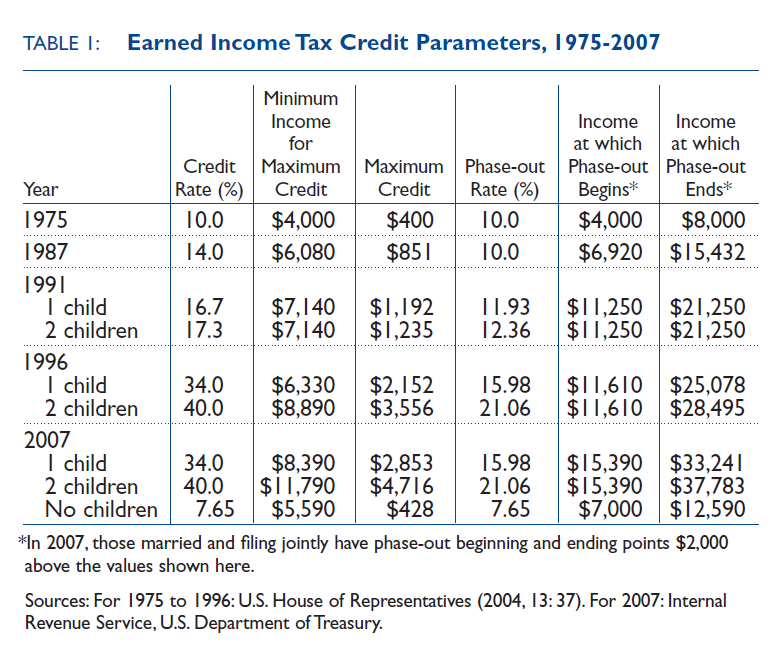

The federal EITC is calculated based upon workers’ earnings and the number of children in their households. The EITC applies at three rates: a low rate of 7.65 cents per dollar in earnings for childless workers, a high rate of 34 cents per dollar in earnings for workers with one child, and an even higher rate of 40 cents per dollar in earnings for workers with two or more children. Workers with no children are eligible for a maximum credit of $41 when their earnings reach $5,380. Workers with one child may receive a maximum credit of $ ,747 if their wage income

reaches $8,080. Workers with two or more children are eligible to receive a maximum credit of $4,536 if their earnings are at least $11,340. For a childless worker, the EITC decreases from its maximum to zero as the worker’s income rises from $6,740 to $1 ,1 0 annually. For workers with children, the credit begins to phase out when family earnings reach $14,810. For families with one child, the EITC reaches zero when family earnings are $3 ,001. For families with two or more children, the EITC decreases to zero when earnings reach $36,348.

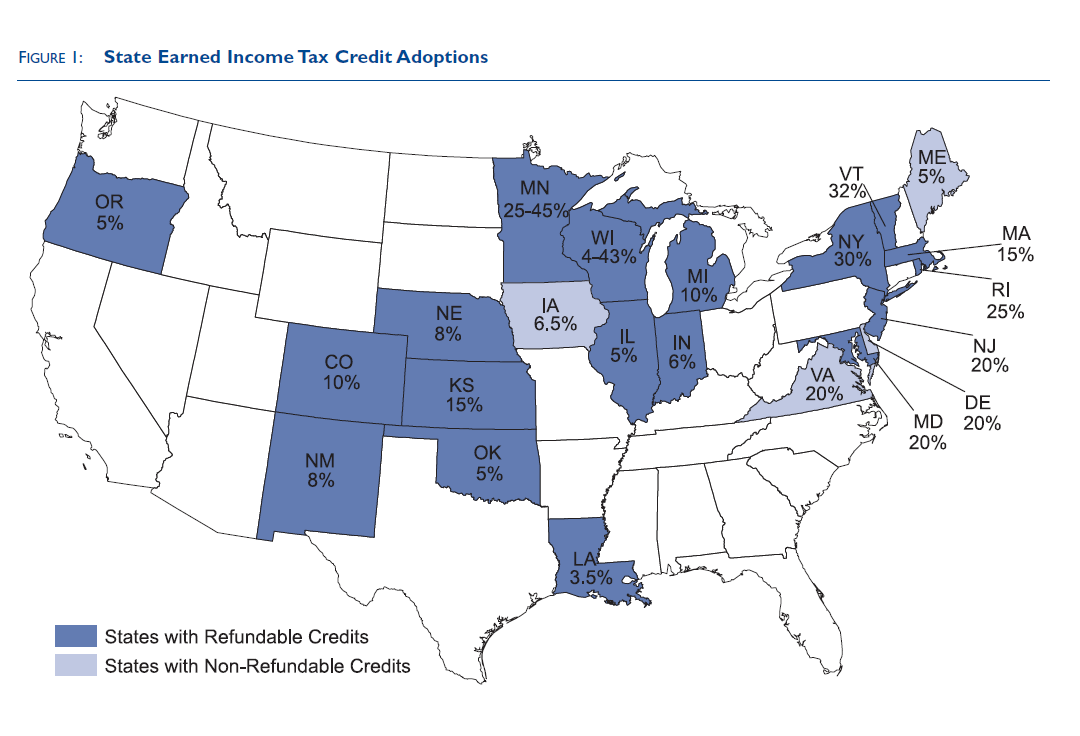

The vast majority of states’ EITCs are calculated as a percentage of workers’ federal EITC . Maine’s EITC is calculated as five percent of the federal EITC . If a Maine worker’s federal EITC is $ 2,000, then his or her Maine EITC is five percent of $ 2,000 or $100. State EITC rates range from a low rate of 3.5 percent of the federal EITC in Louisiana and North Carolina to rates in the range of 30 to 45 percent in Minnesota, New York, Vermont, and Wisconsin. (See figure 1.) After 30 years of experience with the federal and state EITC and a decade after congress enacted major welfare reform legislation, many state policymakers are taking a careful look at how to use their tax systems to encourage work, lower welfare dependency, and help families to achieve economic stability.

The first section of this article describes the federal EITC and its assistance to working Maine families. The second section brings into relief the growth of state EITC and places Maine’s policy in the context of its counterparts across the country. The third section identifies several issues that have developed as both federal and state earned income tax credits have matured. This section describes policy responses that states have engaged to ensure that low income working families receive the maximum assistance possible from the tax credits to which they are entitled.

THE FEDERAL EARNED INCOME TAX CREDIT AND THE GROWTH OF STATE EARNED INCOME TAX CREDITS

In 1975, congress passed the federal earned income tax credit with broad bipartisan support, and the late President Gerald ford signed the policy into law.

Low-wage workers received a credit of 10 cents for every dollar in earnings they reported. Unlike other federal tax credits and deductions, the federal EITC was refundable (see sidebar, page 47). When Congress created the federal EITC , it provided modest income tax rebates to low-wage workers with children, and it offset regressive payroll taxes. In 1975, 6.2 million families claimed the EITC , and the federal government provided $1.25 billion in tax relief, 75 percent of which took the form of refundable tax credits. Families received an average tax credit of $201 ($708 in 2004 dollars). This year nearly 20 million American families will claim the EITC . The overall costs of the credit have risen to $38 billion in 2006, and nearly 90 percent of the costs are cash refunds

to recipients, while the remaining 10 percent are reduced tax payments. The average EITC credit among households with children is $1,784 (U.S. House of Representatives 2004). The federal EITC enjoyed substantial bipartisan support during the 1970s through the early 1990s. Congress enacted expansions of the EITC in 1986, 1990, and 1993. Republican Presidents Ronald Reagan and George H. W. Bush and Democratic President Bill Clinton all signed EITC expansions into law. President Reagan supported the EITC , and the platform adopted by the Republican Party in 1988

explicitly stated the party’s support for the EITC as a means of raising the incomes of the working poor (New York Times 1988). President Reagan recognized that the refundable tax relief, offsetting both income and social security taxes, raised living standards for working poor families, and he recognized that by connecting the EITC to wages, only workers would be eligible to receive its assistance. Because President Reagan had successfully advocated for the EITC to be indexed to inflation, the antipoverty effectiveness and work incentives of the EITC are much more reliable than those of policies such as the minimum wage, which has recently experienced a 12-year period during which Congress did not adjust it to reflect the effects of inflation. In 1993, Congress passed a modest EITC for childless workers to help offset their social security taxes. This final expansion meant that the EITC had grown from a single-rate program to a multiple-rate

program designed to assist workers and their families. Table 1 presents an overview of EITC rates and credit levels and how both have changed over time. These changes effectively made the EITC not only the United States’ largest anti-poverty program, but also its largest work-incentive program. At the time of the 1993 expansion of the EITC , President Clinton stated:

This will be the first time in the history of our country when we’ll be able to say that if you work 40 hours a week and you have children in your home, you will be lifted out of poverty. It is an elemental, powerful, and profound principle. It is not liberal or conservative. It should belong to no party. It ought to become part of the American creed” (MCF 2007: 5).

By the mid-1990’s, the EITC had become the federal government’s largest anti-poverty program for citizens under age 65. As the 1990’s proceeded and the economy continued to grow, an increasing number of states enacted their own earned income tax credits.

These policy adoptions reflected ongoing concerns about living wages for low-income families. State EITC adoptions also helped legislators realign state tax codes that had grown increasingly regressive during the high-inflation periods of the 1970’s and early 1980’s. Congress explicitly encouraged state EITC adoptions when it provided that states could use TANF funds to finance the refundable portion of their state-level EITC’s. Congress included this provision in the Personal Responsibility and Work Opportunity Reconciliation Act of 1996 (PRWORA).

STATE EARNED INCOME TAX CREDITS AND MAINE’S POLICY OPTIONS

Currently, 22 states and the District of Columbia augment the federal EITC with their own earned income tax credits. In the vast majority of states, the state credit is applied to workers’ state income taxes and is calculated as a percentage of the federal EITC . Figure 1 illustrates which states have refundable and which states have non-refundable EITC’s. Among the first states to adopt earned income tax credits were Rhode Island, Minnesota, Wisconsin, and Vermont. Louisiana, Nebraska, North Carolina, and Virginia have been among the more recent states to adopt EITC’s. New York has expanded its EITC frequently, with bipartisan support in its Democratically controlled Assembly, its Republican-controlled Senate, and from former Republican Governor George Pataki.

As the booming economy of the 1990’s roared into the 2000’s, Maine enjoyed a healthy $350 million budget surplus. The Maine Legislature enacted a modest non-refundable earned income tax credit as part of its fiscal year 2001 budget that was approved by Governor Angus King. Maine’s EITC provision provided state income tax relief to low-income Maine families up to a maximum reduction of $215. When it was enacted in the spring of 2000, the Maine EITC cost less than $5 million. The legislature lowered the EITC credit rate from 5.0 percent to 4.92 percent during the fiscal crisis that followed the 2001-2002 recession, and has subsequently restored the rate to five percent.

Maine’s EITC offsets costs associated with working, such as transportation and child care, and, along with the federal EITC , has become a critical ingredient in moving families from welfare to work. Currently, Maine families with incomes below $15,000 annually can claim a maximum state credit of $22 5. Although this reduction is helpful, it effectively raises the disposable income of a full-time worker by only about 10 cents an hour. In states with higher credit rates, such as New York and Vermont, the EITC can raise take-home earnings by as much as 60 cents an hour. Expanding Maine’s earned income tax credit would permit policymakers to help hard-working Mainers achieve a better living standard and lower the tax burden currently placed on Maine workers (OPLA 2006).

An expanded state EITC would provide Mainers with increased incomes that they could then spend in their communities on necessities such as food, rent, and clothing, and on investments in job training and pre- and after-school programs for their children. Studies of families’ uses for EITC reveal that the single payment does not lead to impulsive or frivolous spending. Smeeding et al. (2001) studied families who received the EITC in 1997. Eighty-three percent of families surveyed used a portion of their credits to pay outstanding bills, 74 percent purchased cars or other durable goods, and one-half of all recipients reported using their EITC for savings. Sixteen percent of families benefiting from the EITC planned to use it for tuition and job training, and 20 percent planned expenditures that would enable them to remain in or reenter the work force (Smeeding et al. 2001: 1198). These latter uses reflect commitments to economic mobility and demonstrate families’ willingness to invest their EITC benefits in ways that provide greater economic security or opportunity. Other common expenses for which the EITC provides critical resources have included debt reduction, automotive repair and maintenance, and dental care.

In addition to its positive work incentives, an expanded and refundable state tax credit would direct resources to those parts of the state that are struggling economically. In Maine, EITC receipt is lowest in Cumberland and York counties. In areas with relatively high poverty rates, such as Aroostook, Penobscot, Somerset, and Washington counties, proportionately more families benefit from the federal EITC . Families in these counties would benefit from an expanded state EITC , and local economies would get a boost from these families’ increased incomes.

Of course, it is reasonable to ask how much an expanded tax credit would cost the state. Based upon the current receipt of the federal EITC , a refundable tax credit set at 10 percent of the federal EITC would cost Maine approximately $13 million annually, and a refundable EITC set at 20 percent of the federal EITC would cost the state approximately $27 million annually. Currently, the state spends approximately $5 million annually on its non-refundable EITC , so the net cost of an expanded and refundable state EITC would range from $8 to $22 million. The Maine Legislature could redirect its federal block grant from Temporary Assistance to Needy Families (TANF ) to finance the refundable portion of an expanded state EITC. Currently, Maine spends $140 million annually on its TANF programs. Although a redirection of those funds to a refundable EITC would not be trivial, a refundable EITC set at 20 percent of the federal EITC would require reallocating 15 percent of Maine’s TANF spending. However, unlike many other tax challenges Maine faces, an EITC expansion could be financed not by “trading” one tax benefit for another tax increase or by offsetting a tax credit with spending cuts, but by using available federal resources.

Although a net cost of $10 or $20 million may seem a large amount, given Maine’s fiscal challenges, other state legislatures have decided to enact refundable state tax credits despite similar or larger fiscal challenges. Louisiana, Michigan, and North Carolina have all enacted refundable EITCs, with rates ranging from 3.5 percent to 20 percent, within the last two years.

Michigan and North Carolina have lost thousands of manufacturing jobs in automobiles and textiles, respectively, and Hurricane Katrina devastated Louisiana financially and physically. Nevertheless, in all three states policymakers have viewed the state EITC as a positive tool by which to encourage work and to redirect resources to struggling areas of their states.

EARNED INCOME TAX CREDITS: POLICY PROBLEMS AND HOW STATES CAN HELP

Regardless of whether Maine reshapes its EITC, there are a number of policy issues that could help Mainers receive the full benefits they deserve from the existing federal refundable EITC and the state EITC. The national Governors association has identified three specific issues for states to address to maximize the benefits of the EITC to working families: (1) lack of awareness about the EITC among eligible workers and families; (2) costly tax preparation services and complex filing requirements; (3) costly refund acceleration loans (RALs) offered by tax preparation services.

Recent studies by the Marguerite Casey foundation have estimated that approximately 15 to 20 percent of federal EITC benefits for which families are eligible go unclaimed every year. In Maine, these unclaimed benefits are estimated to be approximately $ 20 million. Maine families and the Maine economy forego these millions of dollars because Maine workers either do not know they are eligible to receive the federal rebate or miscalculate their credits (Mcf 007). A number of states that have not had their own EITC, such as Alabama, Pennsylvania, and Michigan, have initiated EITC education campaigns to raise awareness about the federal program. In 2003, Michigan Governor Jennifer Granholm launched a new web site that provides access to information about the federal EITC and how to claim it. In Louisiana, state government officials have helped create a faith-based partnership to publicize the EITC. In Delaware, state officials have partnered with McDonald’s to distribute information about the EITC on tray liners, and in Illinois participating grocers have publicized the EITC by printing descriptions on grocery bags (nGa 007).

A related problem with the EITC has been that as the program has grown a number of for-profit tax preparation services have targeted EITC recipients as a lucrative business opportunity. In 2005, the latest year for which data are available, EITC benefits averaged approximately $1,734 per family, but tax preparation services charged an average of $100 for each tax return they prepared (Mcf 007). These charges effectively lower the disposable incomes of working families and detract from the EITC’s intended benefits. States have begun to work with a variety of advocacy groups to promote free tax preparation for low-income workers and their families. Illinois, Indiana, Michigan, and Texas all include contact information and locations for free tax preparation. Illinois has dedicated money from its TANF block grant to support its tax counseling Project, which focuses on taxpayers outside Chicago. In 2004, the Illinois government spent $380,000 to complete 22,000 tax returns across 8 sites. This tax preparation cost approximately $17 per return and yielded Illinois residents more than $30 million in federal EITC benefits (nGa 2007). Michigan and Washington have reported similar results. Federal EITC benefits rose 14 to 17 percent in those states after the states created new tax assistance offices. Pennsylvania has provided $ 200,000 in funding for a mobile tax preparation service. This service deploys volunteers with laptop computers to assist families with tax preparation at charter schools, union halls, community centers, and churches.

In addition to its positive work incentives, an expanded and refundable state tax credit would direct resources to those parts of the state that are struggling economically.

In addition to charging hefty rates for tax preparation, many private tax services market refund acceleration loans (RALs) to advance families their EITC benefits. These loans provide a family with an immediate rebate or tax return, but many services charge $100 or more. In many cases, an electronic funds transfer from the federal treasury would occur within two weeks, but the services market the loans as the quickest way to obtain ready cash, and they often charge $100 or more for what is essentially a two-week loan of $ 2,000 or less. These loans carry effective annual interest rates in excess of 100 percent and have raised concerns about the profit taking from a federal program designed to reward work. During the height of tax season, RAL fees can rise to $500, with interest rates effectively reaching 800 percent! As early as 2003, Maine’s senior United States Senator Olympia Snowe called attention to RALs and their costs to families, stating that the IRS had a responsibility to reach out to families to help them claim their full EITC benefit as outlined in the law (Jansen 2003).

The federal EITC has provided state policymakers with an important tool with which to move families from welfare to work.

In response to RALs, a number of states have enacted regulations to limit fees and to encourage tax preparation services to fully disclose taxpayers’ options for receiving the credits. Minnesota, North Carolina, and Wisconsin now regulate tax preparers who offer RALs. In Wisconsin, tax preparers must disclose their fee, refund loans fees, charges for filing, options for filing, anticipated time for credit disbursements, and the RAL interest rate.

DISCUSSION

By using state tax systems to support work and raise incomes, state policymakers can gain the benefit of administrative and policy advantages. Because state EITCs are in the tax, and not the welfare system, the benefits avoid the stigma associated with traditional welfare programs and thus may encourage higher participation. States can target the benefits to focus assistance on particular groups, such as those transitioning from complete welfare dependence to economic independence, and policymakers can dovetail tax benefits with the parameters of their TANF and other workforce development programs. Because wages trigger benefits, program administrators need not monitor beneficiaries for time limits, as they must with TANF receipt. The federal EITC has provided state policymakers with an important tool with which to move families from welfare to work. Without the EITC, the elements of the welfare trap that led to long-term dependency

on AFDC/TANF would remain. Families on TANF would likely find that child-care costs, payroll taxes, and job expenses would offset whatever income increases resulted from leaving TANF in favor of work. With the federal EITC and complementary state tax credits, families are more likely to achieve economic self-sufficiency and decrease their reliance on cash assistance programs like TANF.

By and large, Maine policymakers have provided support for Mainers who work hard but earn relatively low wages. In recent studies, Maine has been identified among the top one-third of states based upon its support for working families, given its resource base (Rodgers 005). At a minimum, Mainers should work together, in both the public and private sectors, to

ensure that working families are receiving the federal tax credits to which they are entitled. More ambitiously, Mainers can consider how best to use effective anti-poverty, pro-work policies that other states have adopted as part of our tax reform and economic development efforts.

REFERENCES

Jansen, bart. 2003. “Many eligible families fail to seek tax Credit: a study finds that half of all Workers Who did Claim the Credit had Paid for tax Preparation and fast cash lending services.” Portland Press herald, January 14, p. 2b.

Marguerite Casey foundation (MCf). 2007. “the earned income tax Credit: analysis and Proposals for reform.” MCf, seattle. http://www.caseygrants.org/documents/ reports/MCf_eitC_Paper.pdf [accessed august 16, 2007]

national Conference of state legislatures (nCsl). 2007. “federal earned income tax Credit: What legislators need to Know.” nCsl, denver. http://www.ncsl.org/ print/wln/eitC.pdf [accessed august 16, 2007]

national governors association (nga). 2007. “state efforts to support low-income families and Communities through the earned income tax Credit.” nga Center for best Practices, Washington, dC. http://www.nga. org/files/pdf/06stateeffortCommunities.pdf [accessed august 16, 2007]

new york times. 1988. “the republicans in new orleans; excerpts from Platform: ‘for our Children and our future.’” the new york times, august 17. http://select. nytimes.com/search/restricted/article?res=fb0717fC3 C5b0C748ddda10894d0484d81 [accessed august 16, 2007]

rodgers, harrell r. 2005. “saints, stalwarts, and slackers: state financial Contributions to Welfare reform.” Policy studies Journal 33(4): 497-508.

smeeding, timothy M., Katherine ross Phillips and Michael o’Connor. 2001. “the eitC: expectation, Knowledge, use, and economic and social Mobility.” the national tax Journal 53(4): 1187-1209.

offi ce of Policy and legal analysis (oPla). 2006. “final report of the study Commission regarding livable Wages.” Maine legislature, oPla, augusta. http://www.

maine.gov/legis/opla/livwagerpt.pdf [accessed august 16, 2007]

u.s. house of representatives. 2004. “2004 green book: background Material and data on Programs within the Jurisdiction of the Committee on Ways and Means.” u.s. house of representatives, Committee on Ways and Means, Washington, dC. http://waysandmeans.house.gov/documents.asp?section=813 [accessed July 18, 2007]